Nickel For Your Thoughts?

Rule Investment Newsletter #16

Nickel Turning a Corner

Nickel is a notorious base metal to invest in, whose cycle oscillates wildly between peaks and troughs, in ways that can be painful and frustrating. The nickel sector is notorious for its boom-bust nature, which sees miners aiming to time investments so they get a few years of great cash generation during the peaks to take them through several years of marginal profitability at best, during the troughs. The tough nature of the nickel business has led diversified miner BHP (LSE:BHP) to seek an exit from its nickel operations. Its Nickel West operation in Western Australia, which includes mines, smelter and refinery, has dragged on its performance for years.

Yet nickel is an essential industrial metal, particularly when added to steel, yielding stainless steel. Its demand has also benefited from the growing fleet of electric vehicles and battery energy storage systems, where nickel provides better energy density, particularly in batteries for long-range or duration, and higher performance. We are presenting nickel as an investment theme, as it is emerging from a trough.

Nickel will be present at the Rule Natural Resource Investing Symposium 6-10 July, in the participation of Centaurus Metals (ASX:CTM) and Bravo Mining (TSXV:BRVO). More than 1,500 investors have already registered to attend in person in Boca Raton, Florida or via our live stream. To join them, click the button below:

Nickel’s Class Divide

Nickel products are generally divided into two categories: Class 1 nickel, with purity above 99.8%, traded on the London Metal Exchange (LME) and used in high‑grade alloys and electronics that typically come from nickel sulphide deposits; and Class 2 nickel, including ferronickel and NPI, used primarily in stainless‑steel and alloy production, with the primary source being nickel laterites. Nickel sulphate, a downstream derivative of Class 1 or intermediate feedstock, represents the battery industry’s essential chemical input. China controls almost 80% of global nickel sulphate refining capacity and has invested heavily to develop capacity and integrated operations in Indonesia.

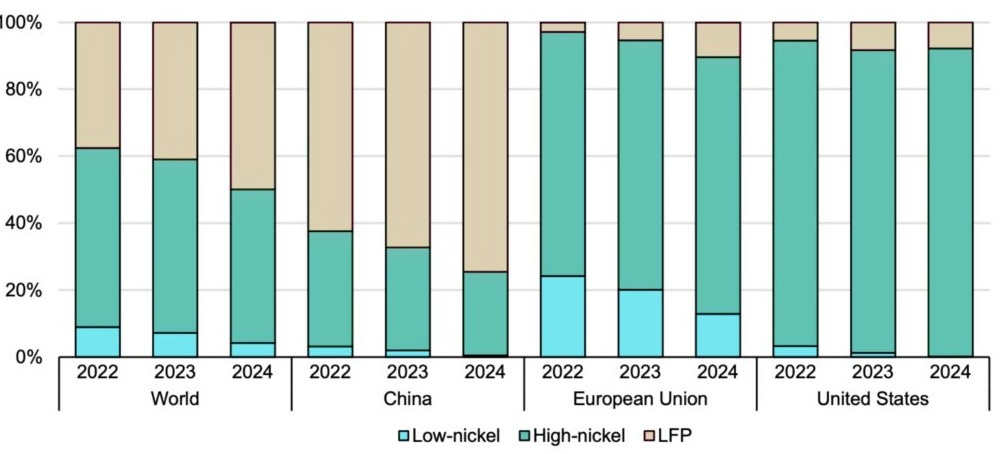

Exhibit 1: Nickel’s share of Electric Vehicle battery sales

Source: IEA & China Automotive Battry Industry Alliance

Asia is the largest consumer of nickel, dominated by China, and the destination for more than 65% of global primary nickel usage, largely in stainless steel. The downstream value-add focus has seen Indonesia rise to become the second largest consumer, having developed a stainless steel industry, followed by Japan. Stainless steel is the largest end-use sector, accounting for about 70% of total consumption. After showing strong potential for nickel use in EV batteries, the market wavered in 2025 amid growing competition from non-nickel chemistries such as lithium iron phosphate (LFP) (See Exhibit 1) and a shift in consumer preference from battery electric vehicles (BEVs) to plug-in hybrid electric vehicles (PHEVs).

The International Nickel Study Group forecast in April 2026 that the 2025 surplus of 283,000t would become a 32,000t deficit in 2026, the first supply shortfall in many years. The INSG said:

“World primary nickel production was 3.88Mt (in 2025) and is forecast to slip marginally to 3.72Mt this year. World primary nickel use is forecast to rise from 3.57Mt last year to 3.75Mt this year.”

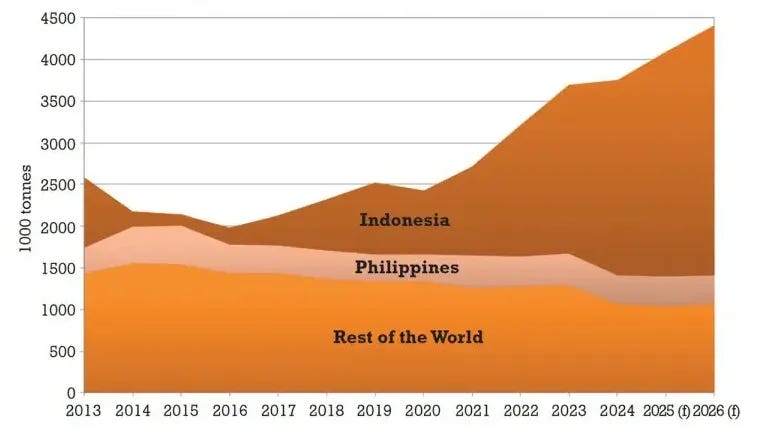

Exhibit 2: World nickel mine production (1,000t)

Source: INSG

Indonesia’s Nickel Pivot

Nickel has been an Indonesian story for most of the last cycle as the country rapidly expanded its production capacity, effectively copying the Chinese model of overbuilding capacity to collapse market pricing and put competitors out of business. This process saw it ramp production from 6-7Mtpy in 2005 to 200Mtpy today (see Exhibit 2). Indeed, much of this capacity was built with Chinese funding to develop an almost captive supply of nickel ore for its own smelters and refiners, as well as for industrial use.

Indonesia (and China) was able to do this because of the vast nickel laterite deposits it hosts on the islands of Sulawesi, Halmahera, and West Papua. Laterite deposits are surface-weathered and tropical, which makes them much easier to mine than the hard rock nickel sulphides found in Canada, such as the class magmatic sulphide Voisey’s Bay deposit in Labrador. However, they are harder to process, either through the high-pressure acid leaching (HPAL) hydrometallurgical process, which uses sulfuric acid at high temperature and pressure to produce intermediate products such as mixed hydroxide precipitate (MHP) or mixed sulphide precipitate (MSP). Or they produce nickel pig iron (NPI).

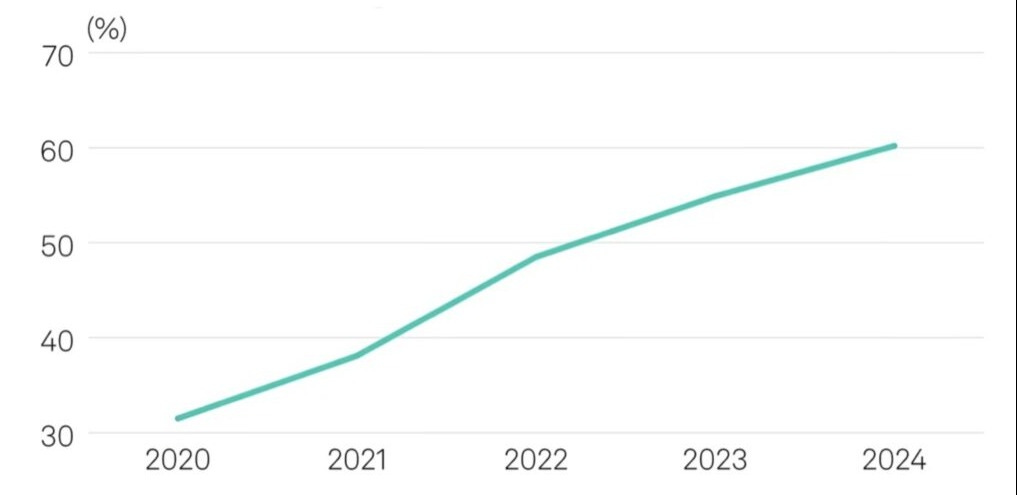

Exhibit 3: Indonesia’s share of global nickel production

Source: S&P Global Market Intelligence

The rapid development of Indonesia’s nickel laterite industry led to prices plummeting amid a surge in new supply. This resulted in the closure of higher-cost operations in Australia and New Caledonia. Indonesia now accounts for 60% of the market (see Exhibit 3), which Mark Selby, president & CEO of Canada Nickel, observes:

“Indonesia is two-thirds of global supply. [Oil cartel] OPEC, at its peak in the 1970s, was only half of the oil supply.”

China was one of the main beneficiaries of Indonesia’s nickel exports, but at a high cost. Nickel laterite miners cleared tropical forests, with environmental impacts similar to those of the oil palm industry: massive deforestation and habitat destruction. The nickel industry was arguably worse than oil palm as there was no sediment control, which destroyed streams with run off, and the processes dumped tailings directly into the ocean. The environmental performance of Indonesia’s nickel industry is one of the reasons Western automotive companies have sought to develop alternative supply lines. Whilst they love the low nickel prices, they can do without the consumer pushback against the environmental destruction that accompanies them.

Things are changing rapidly, though, as Indonesia began applying the latter half of China’s resource development model by raising prices and capturing more value from the business. Indonesia has pivoted from maximising supply to maximising value. Here is Matt Fernley MD at Battery Materials Review and Partner at RK Equity

“The Indonesian government has been pretty consistent: they want to extract maximum value in their own materials, but also don’t want to mine out their resources.”

This led Indonesia to implement a ban on the export of raw nickel in 2020, forcing companies to build smelting and conversion facilities in the country. More recently, it implemented a production quota, cut the duration of a mining license from three years to one, will no longer permit any new HPAL or nickel pig iron projects, and introduced tiered royalty rates tied to nickel prices of $18,000, $21,000, $24,000, and $31,000. The January 2026 quota was reduced by 46% year-on-year. Indonesia is also taking a firmer hand due to the realisation that its nickel deposits are a finite resource, and because the decline in grade is evidence that they have been high-graded. Selby says that 15 years ago, Indonesia had a marginal grade of about 2%. That has now fallen to 1.4% and is trending lower. This grade compression and increasing pricing are making sulphide projects outside Indonesia investible again. Here is Selby:

Laterite deposits are easy to high-grade as they are shallow and on ridges. Miners have been high-grading for 10-15 years. The saprolite ore grade for nickel pig iron fell by 8% in 2025 compared with 2024. They have already mined the best stuff.

The government is also ramping up its environmental policies, particularly regarding deforestation, with fines and the possible loss of concessions for violators. Here is Selby:

“If the Indonesian government creates the conditions in which pricing improves, it is easier to hold miners to account and to put in proper environmental systems, such as drainage channels so that sediment does not enter streams, and to revegetate land more quickly.”

These policies are having success, with the nickel price rising. Here is Martin Turenne, president and CEO of FPX Nickel:

Indonesia is taking a more strategic approach to its position by simultaneously constraining supply and structurally increasing production costs. It is pushing up the global cost curve through stricter environmental enforcement, higher royalties and penalties linked to deforestation and other practices.”

Other factors have contributed to nickel’s price recovery in recent times, principally the Iran Conflict, which has two broad impacts. The closure of the Straight of Hormuz to maritime traffic has sent oil prices above $100 per barrel and constrained supplies. This has increased energy costs across the board, including for the coal that powers Indonesia and its nickel industry. Here is Fernley:

“The coal price is going to go up, and so power prices are going to go up. That is, therefore, going to impact the economics.”

The Iran conflict has also restrained sulphur shipments, which in turn has caused market tightness and higher pricing in the sulphuric acid market. Sulphuric acid is the essential reagent in the HPAL process, with an estimated 10t of sulphur required to produce 1t of nickel. That 10t of sulphur requires 25-30t of sulfuric acid. The Middle East supplies 75-80% of Indonesia’s sulphur supply, according to Indonesia’s nickel smelters association (FINI). China also supplies sulfuric acid to Indonesia, but banned exports from May 2026, and other exporting countries are looking to do so too. Sulphur shortages have forced several Indonesian nickel processors to trim output, reported Reuters. Increasing sulphur and acid costs translate into an estimated $4,000/t of additional cost for Indonesia’s HPAL operations. Together with higher fuel costs, this has been a double whammy for Indonesia’s nickel business. Here is Turenne:

“Average production costs have lifted by an estimated US$2,000–4,000/t over the past six months.”

Nickel is more a supply story than a demand story. While nickel benefits from increasing demand for EVS, that is tempered by the evolution of battery chemistries, with Chinese-made mass market vehicles favouring lithium-iron-phosphate (LFP) formulation rather than the nickel-manganese-cobalt-oxide (NMC). Here is Matt Fernley:

“Demand for nickel from EVs hasn’t been as strong in the last 12 or 18 months, because of the increasing growth in market share of LFP. High nickel batteries dominate in the premium EV space, but in the mass market, you're not really seeing a lot of nickel batteries.”

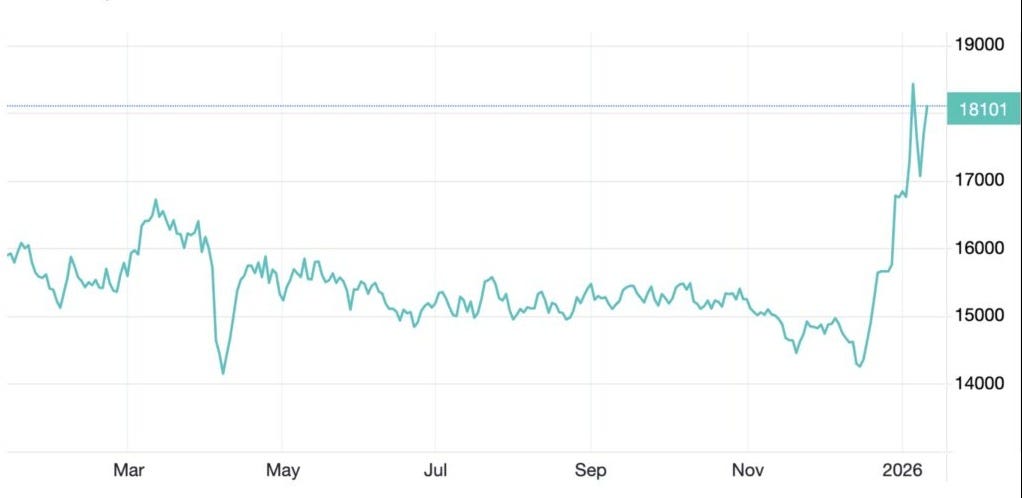

Exhibit 4: Nickel Price 2025-2026

Source: TradingEconomics.com

Indonesia is not alone in looking to obtain more value from its nickel, with the nickel associations of Indonesia and the Philippines signing a MOU on nickel cooperation in May, including the joint development of nickel downstream processing technology. Here is Indonesia’s chief economics minister Airlangga Hartarto:

“The Philippines will no longer be only an exporter of raw nickel ore as it will be integrated into a higher-value regional supply chain, while Indonesia will secure a reliable supply for its battery and stainless industries.”

Nearing Incentive Price

Together, these actions have driven nickel prices from around $15,000/t on the London Metal Exchange to $18,000–19,000/t (see Exhibit 4), indicating the market is now at its incentive price. Here is Turenne:

“We are at incentive pricing in the current market for nickel. With the $17,000-19,000/t range as a new price floor, a project like ours look more attractive.”

In addition to prices strengthening, the Iran Conflict is again prompting the West to rethink its supply chains and how exposed it is to externalities. Consequently, nickel sulfide deposits in Canada are getting a serious look. Here is Selby:

“2026 is a pivotal year for nickel and investors in the space as Indonesia’s focus of growing supply over the past 15 years pivots to managing price to maximize the value they get from a limited resource. There is a big shift in value being captured by Indonesian miners rather than the Chinese processors.”

The Chinese companies that helped build Indonesia’s nickel sector are miffed at Jakarta’s efforts to copy China’s mineral playbook, to their cost. Reuters reports they are now looking to Africa, with Tsingshan Group looking at Madagascar and Lygend Resources at Tanzania and New Caledonia.

Critical Mineral Snooze

There have been a string of supply disruptions that have fueled the critical minerals narrative: COVID-19, the Ukraine war and now the Iran conflict. Each of these has elicited commentary from governments and industry on the importance of having stable, allied sources of raw materials. However, Japan is mainly taking concerted steps to address the issue. Here is Turenne:

“With limited ability to supply its own raw materials, Japan has always looked outwards to secure supply chains with allies and partners. They are far more serious about this and are making funding available to the upstream mining supply chain to secure it, as it is existential for them. North America gets the same wake-up calls but then hits the snooze button and goes back to sleep.”

Western governments have created funding envelopes, such as Project Vault in the US, and have invested directly in specific projects, though this has been sporadic, as when the US government invested in the rare earth company MP Materials in 2025.

Companies

The world’s leading nickel producers in 2025 were Tsingshan Holding Group, Vale, Norilsk Nickel, Glencore, BHP, Jinchuan Group, Nickel Industries, Sumitomo Metal Mining and Eramet. We have already mentioned that BHP is looking to leave the nickel business. It is also worth noting that Norilsk reported a 28% fall in its nickel production in 1Q26, continuing a production slide since 2010. These companies are beyond the scope of this investment, as we look for developers and explorers who can leverage the themes we identify.

Centaurus Metals (ASX:CTM) www.Centaurus.com.au

2026 Rule Natural Resource Investing Symposium participating company.

Australia’s Centaurus is developing the Jaguar nickel sulphide project in the Carajas region of Pará, Brazil, with a deposit hosting 132Mt @ 0.87% Ni for 1.2Mt of contained nickel, for an initial 15-year mine life. Average production in the first seven years will be 22,600tpy at a first quartile AISC of $4.43/lb. The project has an after-tax NPV of US$735M, 34% IRR and 1.8-year payback following an initial capital investment of $380M, of which it has a non-binding offer from Brazil’s National Development Bank (BNDES) for half of that. All key permits have been received and so the mine is ready to build. The company has an initial five-year offtake agreement with Glencore worth US$450M. The company is targeting a FID in 3Q26.

See Rick’s pre-event company interview here.

Bravo Mining (TSXV:BRVO) www.BravoMining.com

2026 Rule Natural Resource Investing Symposium participating company.

Bravo Mining is a Brazil-focused explorer whose Luanga project offers leverage to PGMs, nickel, copper and gold. Bravo raised C$28.5M from Orion Mine Finance in February 2026 to bring its cash on hand to $134M to fund work at Luanga. This includes advancing to a PFS in 3Q26 and, if warranted, toward FS in 2027. A 28,000m drilling program is underway, comprising 22,000m of infill and extensional drilling, and 6,000m of exploration on regional targets, including deep targets beneath Luanga. In January 2026, BRVO was selected as the first mineral project to be designated an anchor tenant of the Export Processing Zone of Barcarena in Pará where the company may develop processing infrastructure to produce metals from Luanga. ZPE Barcarena is an industrial district that hosts fertilizer and chemical producers, many of which rely on imported sulphuric acid. This creates a potential local market for sulphuric acid produced as a by-product of BRVOs smelting process, a more important opportunity given the impact of the Iran conflict on sulphur and sulphuric acid markets.

See Rick’s pre-event company interview here.

FPX Nickel (TSXV:FPX) www.FPXNickel.com

The increasingly positive nickel environment is good news for FPX, which is working to complete a feasibility study for its Baptiste nickel suplhide development project in British Columbia, Canada, in 2028, and take its first steps in the permitting process. Its 2023 PFS detailed the production of 59,100tpy of nickel for 29 years following a $2.2B initial capital investment, using a $19,300/t nickel price. The study outlined a refinery option to upgrade nickel concentrate to produce 40,000tpy of battery-grade nickel sulphate, with incremental capital expenditure of $448M. FPX has yet to decide which route it will follow: focusing principally on supplying the large stainless steel market or also developing refining capacity to supply higher-value-added markets. The company began its formal permitting process in January 2026 and in early 2027 aims to submit its detailed project description. The process will take an estimated four years, unless fast-track initiatives adopted by BC and Canada are applied. The company has received $3.5M through the critical minerals infrastructure fund in 2025. The company has three large corp investors.

“We spent 18 months prior to entering the permitting process having regular dialogue with Critical Minerals Office to get the company, government agencies and the First Nations ready and set the stage for trying to achieve regulatory efficiency,” said Turenne.

Canada Nickel (TSXV:CNC) www.CanadaNickel.com

Canada Nickel aims to have a financing package in place for its C$1.9 billion Crawford nickel sulphide project in the Abitibi region of Quebec by the end of 2026 that seeks to produce 48,000tpy of nickel, 800tpy of cobalt, 13,000oz/y of PGMs, 1.6Mtpy of iron, and 76,000tpy of chrome over 27 years of a 41-year mine life. While it is looking at a traditional 60:40 debt:equity spilt, the company aims to complete the equity portion without having to raise new equity by leveraging funding from provincial, federal and international government lenders, as well as industry. It is looking to raise US$1.5 billion in debt and $1B in equity, including contributions from Samsung SDI, which has an offtake option, and $100-300 million from additional government funding. Another $200 million could come from the G7 group of companies through government agencies in France, Germany, Japan and Korea. Canada Nickel will also benefit from $600 million in investment tax credits under Canada’s Carbon Capture, Utilization, and Storage and Clean Technology Manufacturing programmes. Here is Selby:

“That $600 million is not offset against future income but is a refundable tax credit, whereby when we spend a dollar, the government mails us a check.”

Lifezone Metals (NYSE:LZM) www.LifezoneMetals.com

Is advancing the Kabanga project in Tanzania with backing from Glencore, Taurus Mining Finance, Harry Lundin at Bromma Asset Management & Rick Rule. Kabanga is one of the world’s largest and highest-grade undeveloped nickel sulfide deposits. A FID is anticipated in 2026. The company raised $75 million in 25 to fund pre-FID activities, including early works, such as underground and surface geotechnical drilling to support final design, and site preparation. It has a July 2025 feasibility study for a 3.4Mtpy underground mine, mill and concentrator to produce more than 50,000tpy of nickel, in addition to copper and cobalt for 18 years at an AISC of $3.36/lb following an initial capital investment of $942 million. The project will yield an after-tax NPV8 of $1.58B, a 23.3% IRR, and a 4.5-year payback, based on long-term consensus metal prices of $8.49/lb for nickel, $4.30/lb for copper, and $18.31/lb for cobalt. The Government of Tanzania has a 16% free carried interest in the project, which provides it with a degree of political stability; however, the company is seeking a partner after 17% former partner BHP walked away in July 2025, having invested $100M in the project and its hydrometallurgical ore processing technology. As noted, BHPO is looking to exit the nickel business. Lifezone is working with Standard Chartered Bank to find a new partner. A key attraction of Kabanga is that it is not in Indonesia.

Here is CEO Chris Showalter speaking to the leading mining publication in October 2025 Mining Journal:

“So that’s why Kabanga, as a scalable, sizable alternative, becomes strategically very important to the discussions we’re having with Western governments, not only the US.”

Reuters reports that Lygend Resources is making overtures to buy into LZM and/or Kabanga LZM declined to comment other than saying that it is negotiating for a potential strategic investment into Kabanga, having received multiple offers.