Paul's Notes #4

Consequences of Consequences

With the world’s eyes on the Persian Gulf, this issue of Paul’s Notes looks at some of the potential consequences of the conflict between the US and Israel, and Iran.

I think many were surprised that a bigger conflagration did not kick off in July 2025 when the US and Israel bombed Iranian nuclear installations. Back then, both sides were feeling each other out. Israel and the US wanted to see if and how Iran would respond. Iran sent missiles into Israel, and it would be interesting to see how Israel would respond. The US was not positioned to enter a larger conflict with Iran in 2025. Even in January, when Iran killed 30,000 of its people to suppress protests, the US was not yet ready. In January, President Donald Trump told the Iranian protestors that help was on its way. As February ended, the US was in a position to act, with the USS Abraham Lincoln and USS Gerald R. Ford carrier groups in place.

President Trump has said that the action will take at least a month. War always depends on supply chains, and in this instance, who will run out of missiles first, and to what extent Israel will stomach the bombardment it is receiving in the meantime.

The US has sent an unequivocal message that Iran will not develop nuclear capability, and to that end, it seems bent on effecting regime change. Regime change in Iran will be a harder task to accomplish than in Venezuela. A regilous, fundamentalist regime has spent about 50 years entrenching itself, and will be difficult to root out. It didn’t flinch at killing 30,000 of its own people. Taking out the head honcho did not result in regime collapse as in Iraq with Saddam Hussein, Libya with Muammar Gaddafi, Syria with Bashar al-Assad, or Venezuela with Nicolas Maduro. These were despots who ruled by fear, but without the fervour of religious zeal of their supporters to stand firm behind them. Let’s look at some of the consequences.

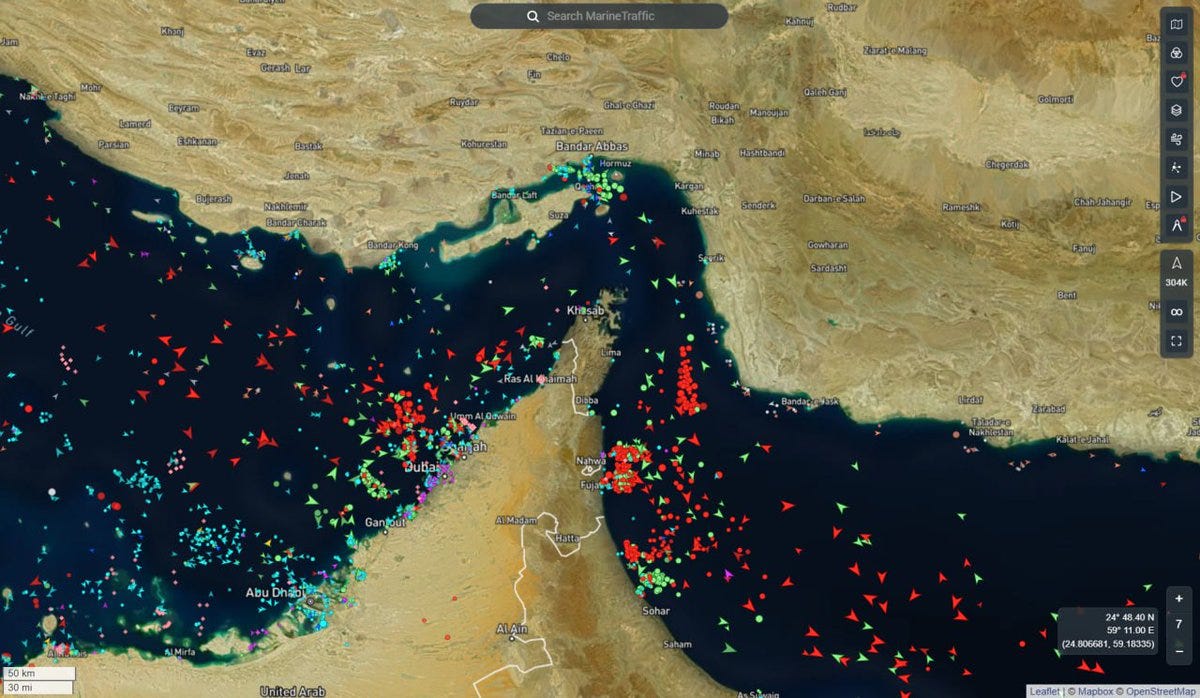

Oil

The oil price has steadily climbed since the conflict began, and it became clear that shipping through the Straight of Hormuz would be reduced. Some 20% of the world’s oil passes through this channel at a rate of about 100 tankers per day. Most of this goes to India, China and Japan. The tankers are sitting at anchor (see image above), not because of the direct threat of attack, although this is happening, but because insurance cover has been suspended or terminated. The oil price has risen by about 30% over the past week, from around $65 per barrel to more than $100 per barrel. With shipping stranded, Gulf oil production is being pared as there is nowhere to store it. The banks have forecast oil prices will increase to triple digits, with JP Morgan suggesting $120-130 per barrel.

What is the US 5th Fleet doing? The US 5th Fleet, based in Bahrain, is tasked with ensuring the free flow of commerce through the Straight of Hormuz, but has yet to step up to the plate. This is because the nature of naval warfare has changed and become asymmetric. Ukraine has shown the massive impact relatively cheap naval drones can have on traditional battleships, having destroyed or disabled a significant portion of Russia’s Black Sea Fleet, including the sinking of the guided-missile cruiser Moskva in April 2022. The US does not want that to happen to the 5th Fleet, and so it has held its distance so far.

Let’s look again at the chain of events through a wider lens to see how things may play out. A leading news story in 2025 was the US attacking and destroying speedboats in the Pacific Ocean and Caribbean Sea that were alleged to be carrying drugs. This was not a Crockett and Tubbs Miami Vice redux, but a live-action rehearsal for the main event: destroying Iranian naval drones to keep the Straight of Hormuz open and protect the 5th Fleet. The action to remove Venezuela’s president Maduro can also be seen as a preparation for war with Iran, as it secured US supplies of oil. The US is relatively unaffected by shipping problems in the Gulf.

Rick cycled into some blue-chip oil names like Exxon in October 2025, viewing $60 per barrel oil prices as a floor with the potential to increase by 30%. However, his timeframe back then was in two to three years. Higher oil prices will also benefit the Canadian oil and gas companies we discussed in RIN #1.

Copper and fertiliser

Robert Friedland has posted on how reduced Gulf oil production and shipping will reduce the supply of sulphuric acid. The Gulf region accounts for 50% of the world's sulphur supply. He said much of this will go to Africa’s copper producers, which means they will face higher costs and potential production restrictions if they cannot obtain the acid they need. This may not have as much impact on copper prices as it might have, given that China set its lowest GDP growth target since 1991 at 4.5-5% in its latest five-year plan, published during the first week of March. China is the world’s leading consumer of copper, and a slowdown in its growth will lead to lower copper consumption.

A twist in the copper tail is that Iran has targeted commercial datacentres in the UAE and Bahrain, with Iran’s Islamic Revolutionary Guard Corps claiming the attacks aim to reduce the military and intelligence activities of the US and Israel in the region. Whatever the reason, data centre construction requires a large amount of copper.

Shipments of nitrogen fertiliser urea are also impacted. The region accounts for 34% of the world's urea production, with much of it coming from Iran. Urea prices have increased by about 30% since the start of the conflict, according to Argus Media. The region also produces other fertiliser chemicals, such as ammonia and phosphate. Lower fertilizer shipments ultimately affect food production worldwide. This disruptions follows that of the Russia-Ukraine, which also impacted fertilizer shipments and production due to interruptions to Black Sea shipping.

Critical minerals

Donald Trump has spent much of his second administration talking about building inventories of critical minerals, and now he is sending those inventories to Iran. Beyond this flippant comment is an important consideration. The ordinance being deployed can do what it does because of tungsten, antimony, heavy rare-earth elements, gallium, copper, silver, and many other geological oddities. Returning to the point that most wars are won by those who have the best supply chains, this conflict is set to suck in large amounts of critical minerals, and once it ends, even more to replace the materiel that has been spent. There has been much debate on social media about how much silver is used in Tomahawk cruise missiles. CPM Group estimates the number at 10-15oz, with the use of silver in missiles is measured in hundreds of thousands of ounces over the past 40 years.

The extent of the potential commodity impacts will depend on the duration of the conflict, but the criticality of critical minerals will become even more pressing as military restocking occurs during and after the conflict has ceased.