Paul's Notes #5

Going, going, gold

With the first mining investment conference season now in the rearview mirror and the 2025 financial reporting cycle completed, I have crunched some numbers to get a view on the health of the gold sector. The analysis focuses on US- and Canadian-listed gold companies. The analysis shows a shiny, happy picture, but geopolitical events have moved rapidly since the end of 2025, taking the shine off precious metals in the short term.

The macro-economic scenario has changed rapidly since the start of March, with the US and Israel entering into a conflict with Iran. This has seen the gold price shed more than US$1,000/oz and energy prices jump 40%, neither of which are good for miners.

Rick and I spoke at length about some of the potential implications of the Iran conflict in this video recorded for Kitco Mining on March 19th.

As a reminder, the 2026 Rule Symposium in Boca Raton, Florida, will be held from July 6 to 10, 2026. The viewpoints of the extensive panel of macro experts may never be more crucial for inverstors seekign to navigate current market conditions than at the current time. To register, click the button below.

Happy, Happy, Joy, Joy

Gold companies had a bumper 2025, with many posting record earnings, record free cash flow and record shareholder returns, although production was generally flat, as costs continued to creep upwards.

Production

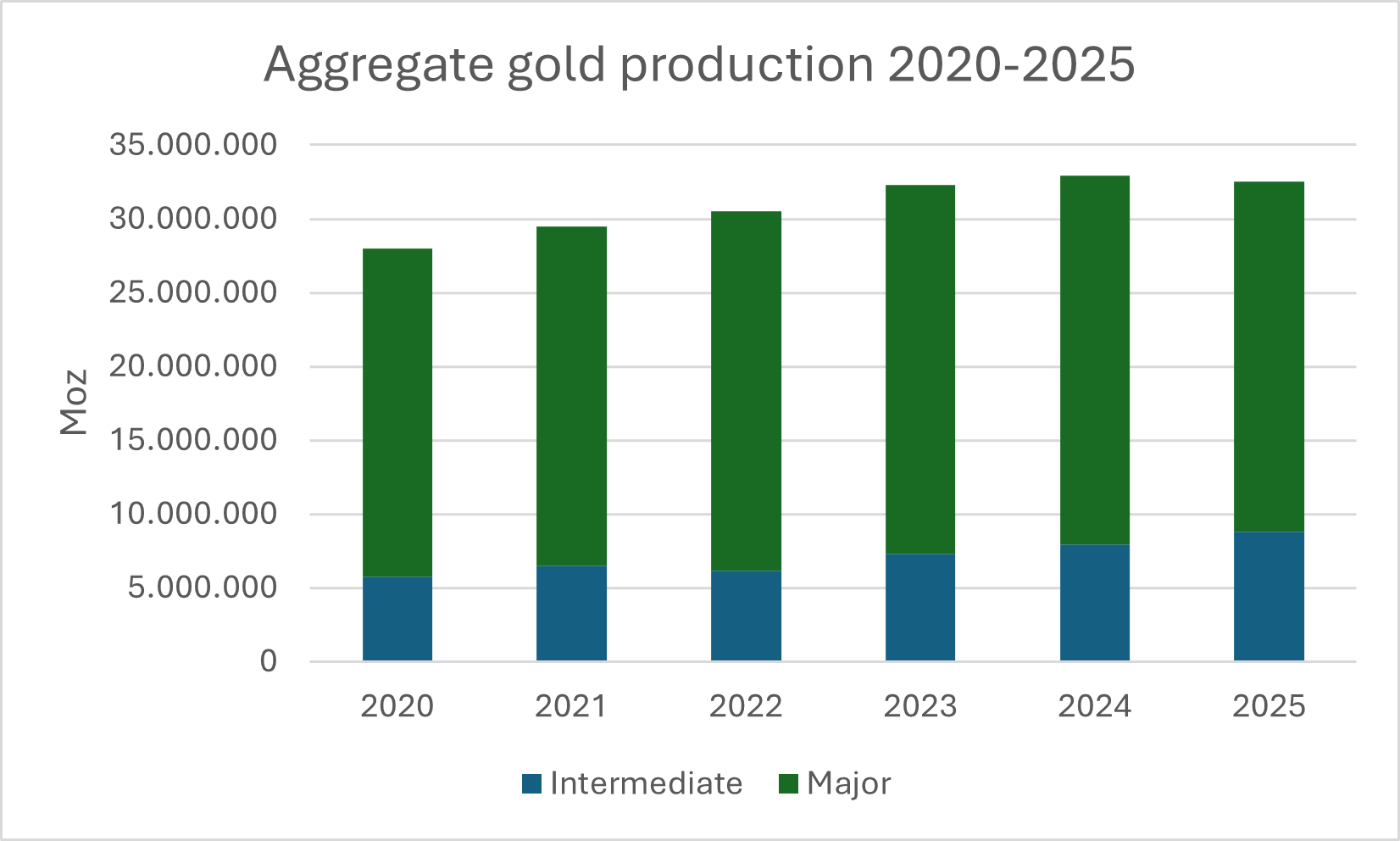

Gold production continued to track sideways in 2025, with output from the major producers dipping by 5% to an aggregate 23.7Moz of gold equivalent compared with 25Moz in 2025. This fall reflects the divestment of assets from Newmont and Barrick Mining, as seen in the 10% increase in production by the intermediate companies to 8.8Moz from 7.7Moz in 2024.

Newmont’s 2025 output fell by 13% to 6Moz, partially as a result of divestitures, while Barrick’s fell by 24% to 3.5Moz. Pan American Silver also saw a double-digit decline of 13% to 1Moz. In the plus column were B2Gold with a 22% increase to 980,000oz, Gold Fields with an 18% increase to 2.4Moz, and AngloGold Ashanti with a 16% increase to 3.1Moz.

Among the intermediates, production growth was led by Equinox Gold at 48% to 923,000oz, reflecting the acquisition of Calibre Mining; Coeur Mining at 32% to 633,000oz, reflecting the acquisition of Silvercrest Metals; and Aris Mining at 22% to 256,000oz. On the negative side, Fortuna Mining saw a 30% fall in production to 317,000oz and Centerra Gold a 25% fall to 342,000oz.

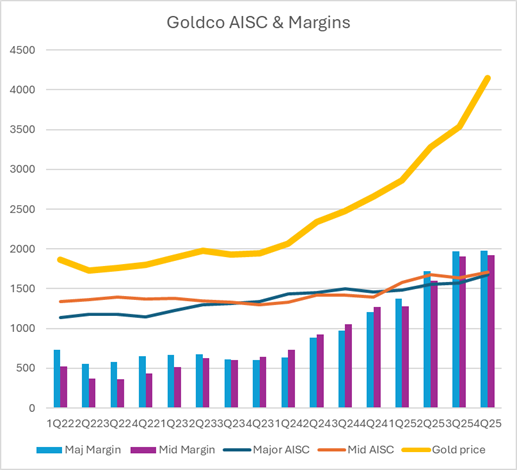

AISC

Costs continued to increase in 2025 with the majors seeing their all-in sustaining costs (AISC) increase by 11% to US$1603/oz. Despite this, higher gold prices led to an increase in the average AISC margin from 46% in 2024 to 58% in 2025. Leading the pack was Agnico Eagle Mines at 61%, and bringing up the rear was Gold Fields at 44%. Four companies saw double-digit AISC increases: Gold Fields (18%), Endeavour Mining (18%), Kinross Gold (13%) and Barrick Mining (10%). Increased fuel and sulphuric acid costs may increase AISC in the near term.

Among the intermediates, the average AISC increased by 19% to $1648/oz, but the average AISC margin rose from 42% in 2024 to 53% in 2025. Leading the pack was Artemis Gold at $869/oz and Lundin Gold at $1015/oz. Bringing up the rear were SSR Mining ($2153/oz) Allied Gold ($2057/oz) and Mineros ($2032/oz). This data includes estimates and assumptions for New Gold, which was acquired by Coeur Mining and did not report full-year 2025 figures.

Almost all the intermediates posted double-digit increases in AISC. The exception was Equinox Gold, which reported a 3% AISC increase. A number of companies saw significant increases in AISC, including Torex Gold (54%), Centerra Gold (41%), Mineros (31%), Eldorado Gold (29%) and DPM Metals (29%).

Iran

With the gold price having lost more than $1000/oz at the time of writing since the start of the Iran conflict, and energy prices, which constitute 20-40% of mining costs, increasing significantly, some analysts suggest AISC could increase by $200/oz just from higher energy prices. A lower gold price and higher cost scenario could make the margins of the worst performers in the sector start to look a little threadbare if the conflict continues. Companies may respond by cutting exploration budgets and reining in sustaining capital expenditure.

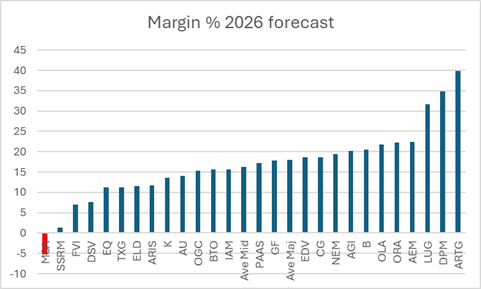

I ran a very crude analysis to see how resilient goldcos would be with this negative $1200/oz swing, using the full year and fourth quarter 2025 AISC, as a basis, assuming the current gold price of $4,500/oz holds for the rest of the year, which is about $1000/oz higher than the average price for 2025. This showed a handful of companies with sub-30 % AISC margins, but generally, companies would maintain a gold level of profitability. However, looking at what further deflation of the gold price could mean, by running the higher AISC numbers at the 2025 average gold price, the wheat starts to separate from the chaff.

If the gold price averages the same as it did in 2025, $3440/oz, we see a very different picture with four companies with a single-digit AISC margin and one, Mineros, having a negative margin. Another $1,000/oz fall in gold would be very problematic for the gold sector and would definitely impact what we will discuss in the next section.

The golden lining to this would be if the Iran conflict is a short-term affair, the Strait of Hormuz reopens to energy shipments, energy prices fall, and a business-as-usual scenario returns. In this instance, the higher-cost producers who are being pummelled more than average today would have the greatest leverage to rising gold prices tomorrow.

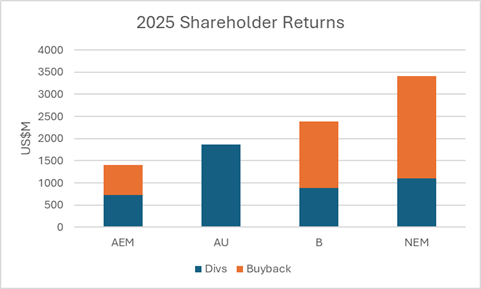

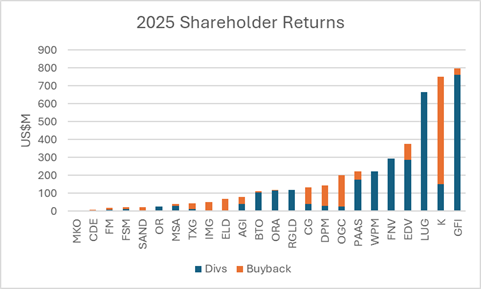

Shareholder returns

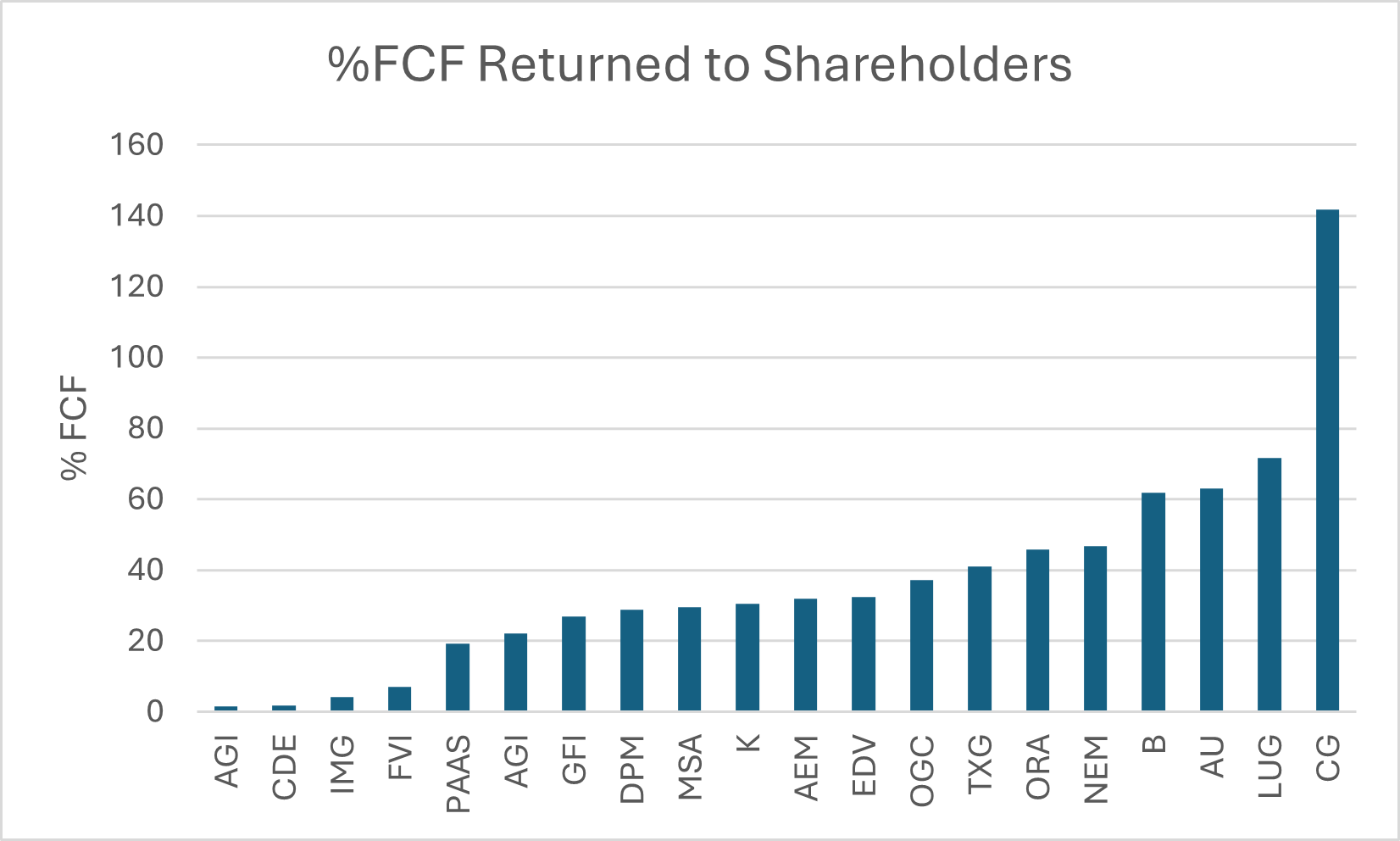

Mining companies generated almost $32B in free cash flow (FCF) in 2025 and returned an average of 38% of FCF to shareholders, led by Lundin Gold at 72%, AngloGold Ashanti at 64%, and Barrick Mining at 62%. These figures do not include New Gold or Allied Gold, which were subject to takeovers and did not report full-year 2025 FCF figures.

At least 13 companies increased their dividends in their 2025 results announcements, with at least four announcing the initiation of dividends.

Capital returns to shareholders from miners, royalty, and streaming companies increased by 95% in 2025 to $13.6B from $7B in 2024. Newmont led capital returns with $3.4B in 2025, followed by Barrick at $2.4B, AngloGold at $1.9B and Agnico at $1.4B. Dividends accounted for 57% of returns, or about $7.7B, down from 69% in 2024. Buybacks increased to 43% of the total from 31% in 2024.

Conclusion

The current pullback in metals and prices and company share prices is a very real stress test for investors, and things could get worse before they get better. A longer-term view shows that the macroeconomic case for gold remains strong, and, if anything, strengthens it: War is expensive, so the US debt will grow; War is inflationary, so the prospect of the US Federal Reserve cutting interest rates quickly and deeply is hard to countenance.