Paul's Notes #7

1Q26 results to fuel goldco M&A?

Way back in RIN #3 we looked at Gold M&A, a topic we are reprising here in Paul’s Notes form to reflect on what we learned from the 1Q26 goldco financial results, and as we look forward to the Rule Symposium 6-10 July, where a number of companies that could be on either side of an M&A deal will be participating. To share this post, please click the link below.

Gold producers that will be attending the 2026 Rule Symposium include the following. Click on their name to see Rick’s pre-conference interview:

Agnico Eagle Mines / Aris Mining / Contango Silver & Gold / Dundee / Helius Minerals / Hemlo Mining / I-80 Gold / Luca Mining / McEwen Mining / Mineros / OceanaGold

Gold developers that will be attending the 2026 Rule Symposium include the following. Click on their name to see Rick’s pre-conference interview:

Banyan Gold / Collective Mining / Dakota Gold / First Mining Gold / GoGold Resources / New Found Gold / Revival Gold / Seabridge Gold / Skeena Gold & Silver / Snowline Gold

More than 1,500 investors have registered to attend in person in Boca Raton, Florida or via our live stream. To join them, click the banner above or the button below:

What are the 1Q26 takeaways?

Sector leader Newmont (NYSE:NEM) announced an astonishing record net profit of US$3.3B, an increase of 74% year-on-year, compared with $1.7B for Agnico Eagle Mines (NYSE:AEM) (+108%) and $1.6B for Barrick Mining (NYSE:B) (+238%).

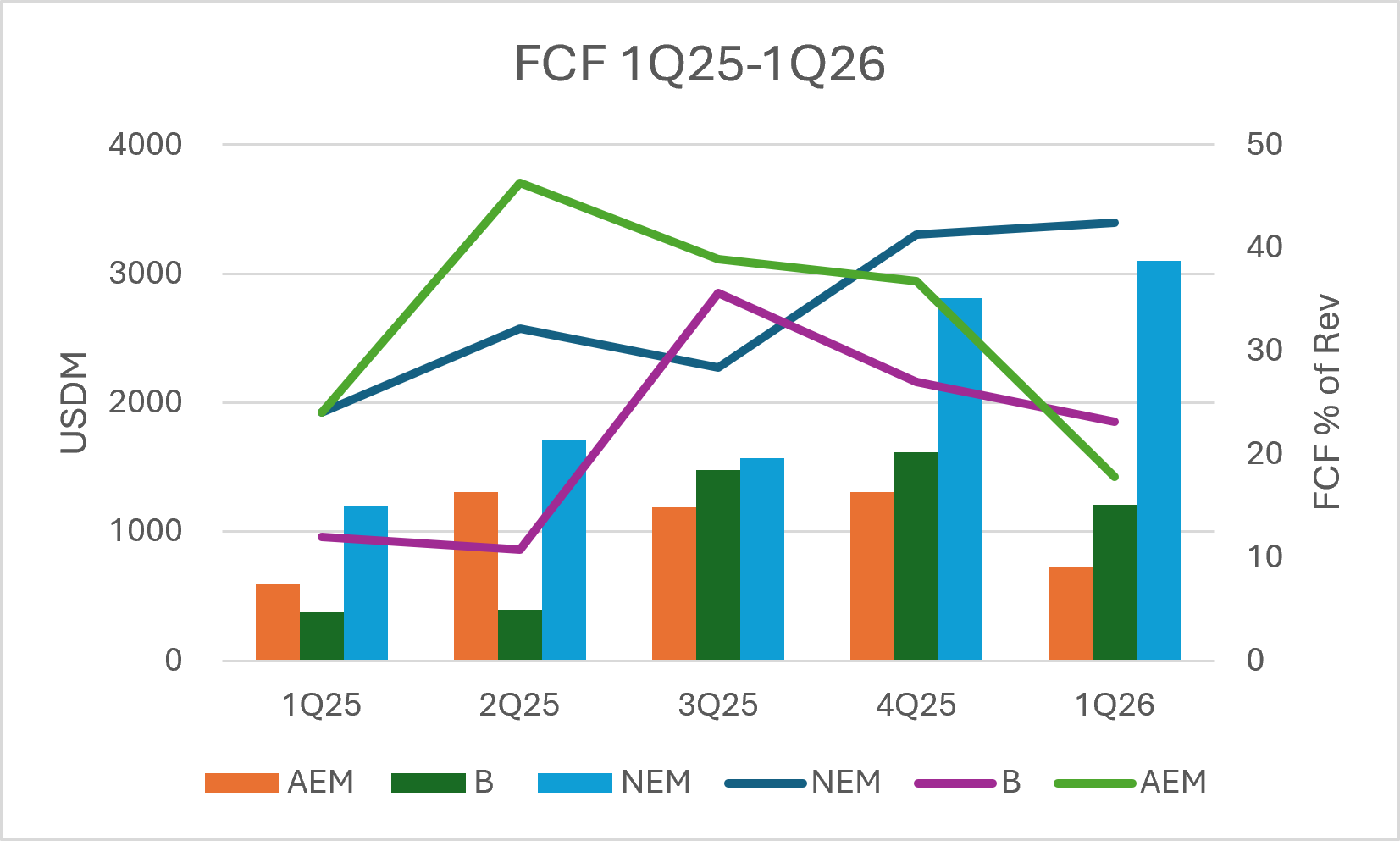

NEM generated record free cash flow of $3.1B, some 42% of revenue, which was up 10% on the quarter and 157% on the year. AEM saw its FCF fall 44% on the quarter to $732M, some 18% of revenue, although it was up 23% on the year, while B saw its FCF fall 25% on the quarter to $1.2B, some 23% of revenue, although up 223% on the year.

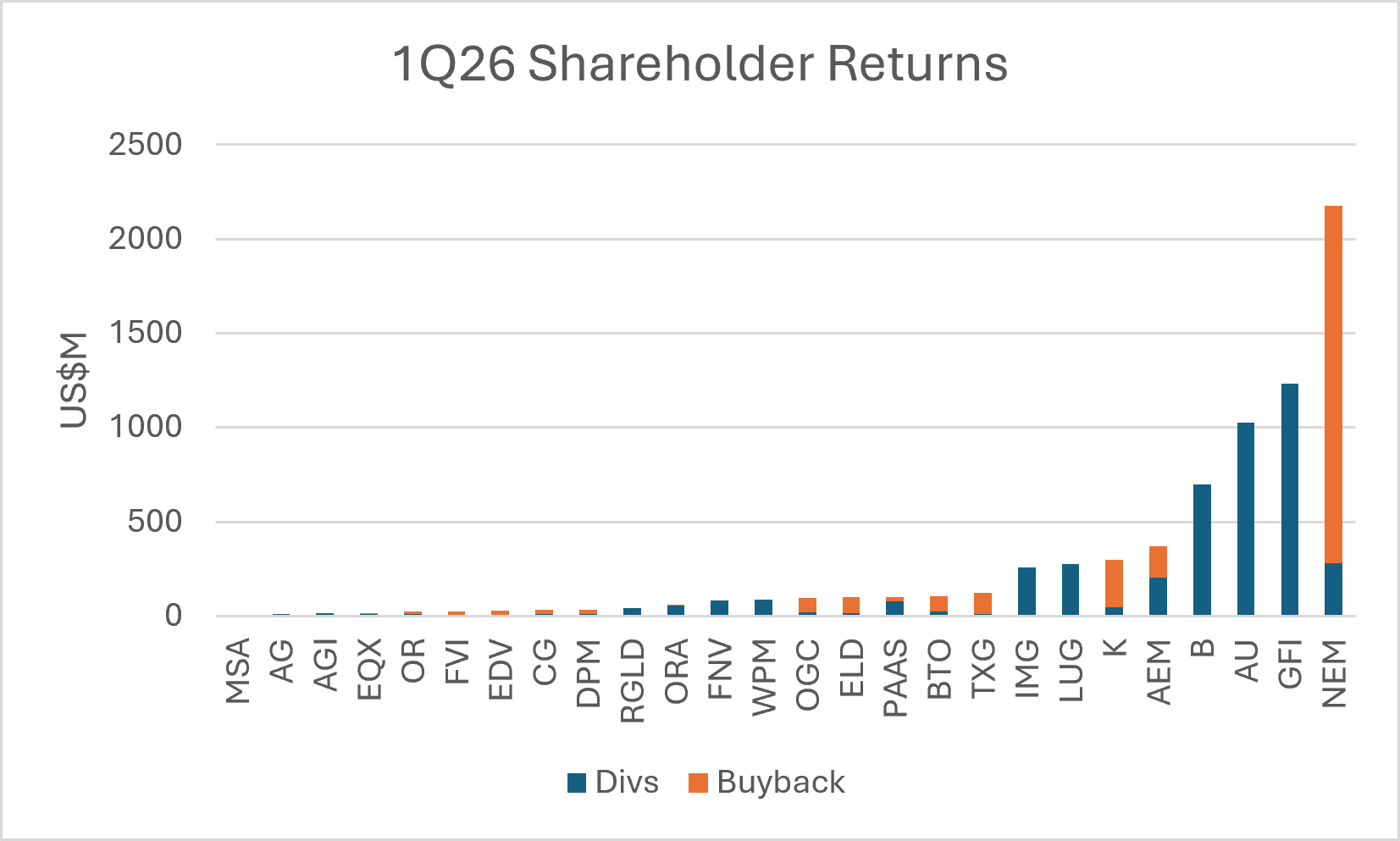

NEM returned $2.2B to shareholders in the quarter, accounting for 70% of FCF, with dividends of $282M and share repurchases of $1.9B. B returned $697M, some 58% of FCF, all in dividends, while AEM returned $371M, 51% of FCF, with $202M in dividends and $371M in buybacks. B and AEM faced stiff competition from AngloGold Ashanti (NYSE:AU), which returned $1B, some 88% of FCF, in dividends, and Gold Fields (NYSE:GFI), which returned $1.2B in dividends.

Aggregate shareholder returns for the companies surveyed totalled $7.3B in the quarter, comprising $4.5B in dividends and $2.8B in buybacks, putting the sector well on its way to eclipsing the $13.6B paid out in 2025.

AISC

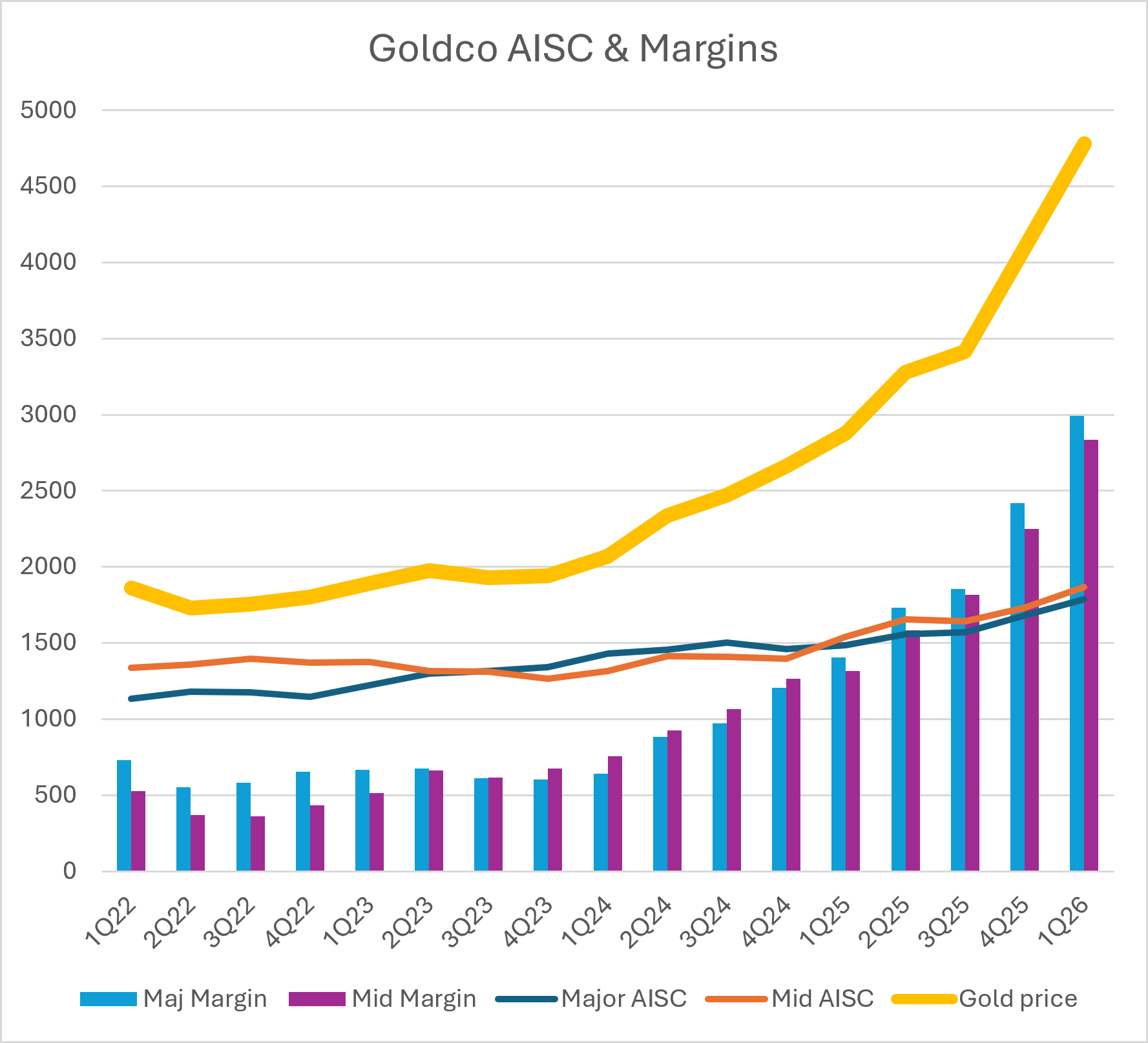

Costs continue to rise, but at a slower rate than metals prices. The senior gold producers averaged an all-in sustaining cost (AISC) of $1788/oz in the quarter, a 6% increase over the December 2025 quarter and 22% increase over the prior year, for an average margin of 63%, some $2994/oz. AEM leads the major gold producers at $1483/oz, giving it a margin of 69.5%, with B and NEM virtually equal at $1708/oz and $1709/oz, respectively, although NEM obtained a higher margin at 65.1% to B’s 64.9%. In dollar terms, the margin was $3378/oz for AEM, $3191/oz for NEM and $3115/oz for B.

The mid-tier producers saw their aggregate AISC increase to $1868/oz, an average increase of 10% on the quarter and 27% on the year. This resulted in an average margin of 62%, or $2843/oz.

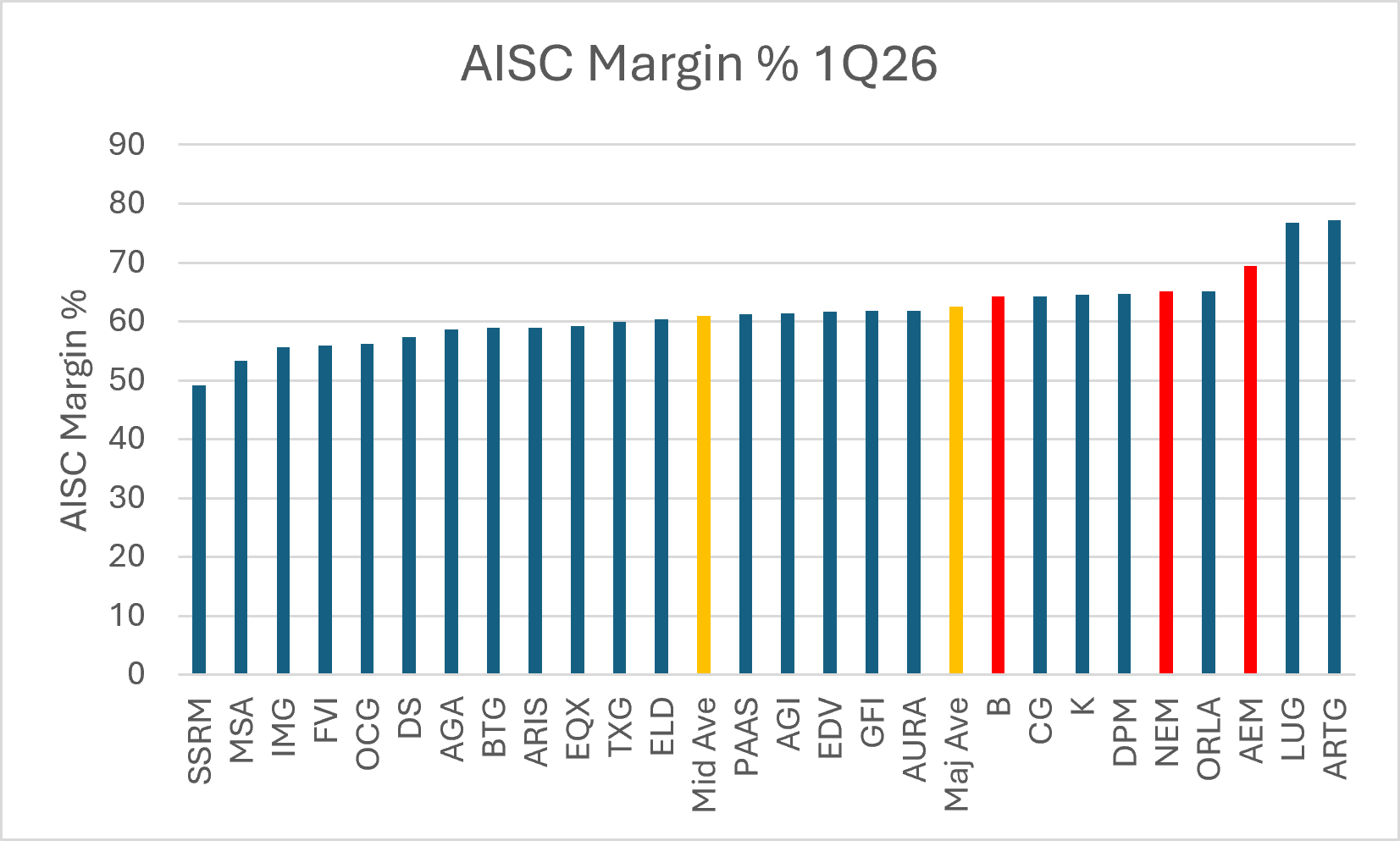

The leading producers now have comfortably higher margins than their peer group average of around 60%. What is more useful for an investor, however, is to see changes in relative performance, and whose is improving most. Among the majors, Kinross Gold (TSX:K) saw a 15% quarter-on-quarter margin increase to 64.5%. Among the mid-tiers, Mineros (TSX:MSA) saw a 36% margin increase to 53.3%. In dollar terms, B saw a 173% year-on-year increase in its margin, with strong performance by NEM (+147%) and AU (+134%). Among the mid-tiers, standouts were Iamgold (TSX:IMG) (+232%), Equinox Gold (TSX:EQX) (+230%) and Alamos Gold (TSX:AGI) (+$198%).

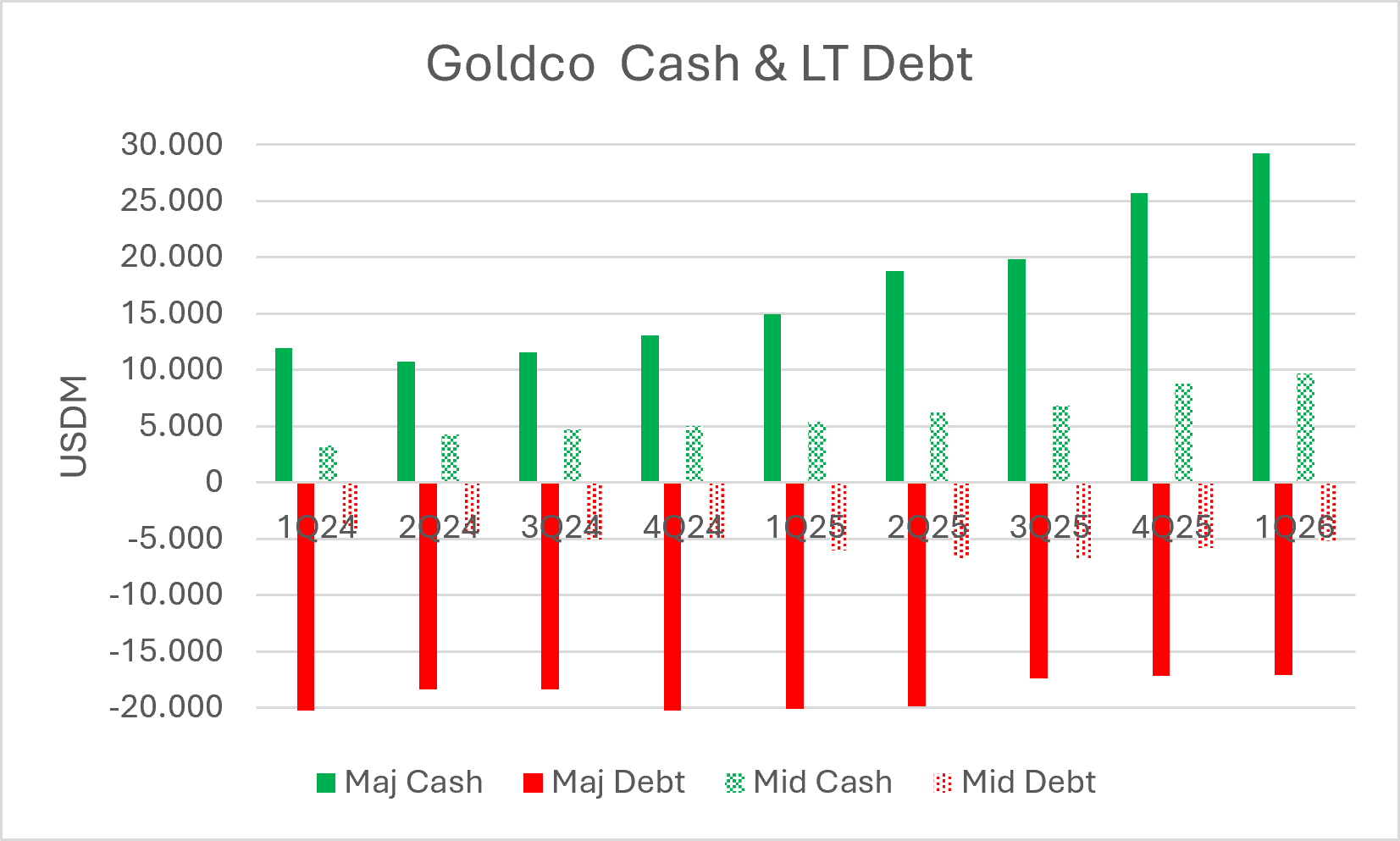

In addition to increasing shareholder returns, the cash generation in this market is enabling companies to build their treasuries and, to a lesser extent, pay down debt. Many companies refinanced their debt several years ago to take advantage of the extremely low interest rates then available, while also pushing debt repayment out. This explains why the aggregate debt of the major miners has remained relatively constant over the past two years. The debt is easily serviceable with their growing income, and they prefer to build cash and improve returns to shareholders, paying debt only as it matures rather than accelerating its repayment.

With debt in a comfortable position, the majors have doubled their cash holdings in the past two years to almost $30B. This matters because gold production continues to track sideways, meaning that at some point, gold producers will likely have to turn to M&A to replace depletion, as few companies can do so through exploration. Mid-tiers are also increasingly cashed up and will likely turn to M&A as they seek to break out from the pack through growth. A reference here is the recent announcement that EQX will acquire Orla Mining (NYSE:ORLA).

For the record, in 1Q26, output from the major producers slide 8% to an aggregate 5.6Moz of gold equivalent compared with 6.2Moz in 4Q25, although it was up 14% from the 5Moz a year ago. This fall reflects the divestment of assets from NEM and B, as seen in the 9% year-on-year increase in production by the intermediate companies to 2Moz from 1.8Moz, although this slid 20% from the 2.4Moz achieved in 4Q25.

M&A will be one of the topics under discussion at the 2026 Rule Symposium. To attend via our live stream, click the button below:

IPO

An addendum to our recent IPO issue of Paul’s Notes #6. Sunshine Silver Mining & Refining (NYSE:SSMR) is to IPO 20M shares on NYSE @ up to US$16.50 to raise $330M, under the ticker SSMR (not to be confused with SSR Mining’s SSRM ticker). SSMR aims to bring the permitted Sunshine Ag mine in Idaho’s Coeur d’Alene district back into production. The Electrum Group will retain more than 50% ownership. SSMR could achieve a valuation of $2.32B, or $7.50/oz for its 300Moz, which would put it well above its peer group, according to analyst Don Durrett. Durrett said Honey Badger Silver (TSXV:TUF) has 400Moz and $1.45/oz valuation, BMC Minerals (ASX:BMC) has 400Moz and a $1.68/oz valuation, Vizsla Silver (NMYSE-A:VZLA) has 360Moz and a $3.60/oz valuation, and Blackrock Silver (TSXV:BRC) has 120Moz and a $3/oz valuation.