Silver Bull Running

Rule Investment Newsletter #7

Silver can be a perplexing and frustrating metal to invest in as its comportment flips between an industrial and monetary metal. It can also be highly profitable if you get your timing right and you understand some of its fundamentals. With that in mind, and with its price starting to run, silver is the subject of this investment theme.

For a deep dive into silver investment, the Rule Classroom Silver Bootcamp is still available.

As an industrial metal, silver is unique due to its characteristics that are valuable in diverse ways. It is very electrically conductive and reflective, and finds new uses in the energy transition. While total silver fabrication demand has remained relatively flat for the past 25 years, photovoltaics have grown from nothing in 2020 to more than 130Moz today, with another growing market in EVs. Here is what Randy Smallwood, president and CEO said in the Rule Silver Bootcamp.

“Silver not only has the same investment criteria, the same score of value capabilities, the same measure of value capabilities that gold has had for 1000s of years, but it has physical attributes that really fit into today's world.”

There are a lot of source materials about silver’s industrial uses and its market, particularly from The Silver Institute and CPM Group.

Silver’s ability to generate phenomenal returns makes it a subject of this investment theme, particularly as we see favorable conditions for the metal ahead. We sense we are on the cusp of an important inflexion in the market, as we are very likely to be in a US dollar bear market, which makes for very fertile conditions for precious metals bull markets. If we are right about the deterioration of the purchasing power of the US dollar, this precious metals bull market has legs.

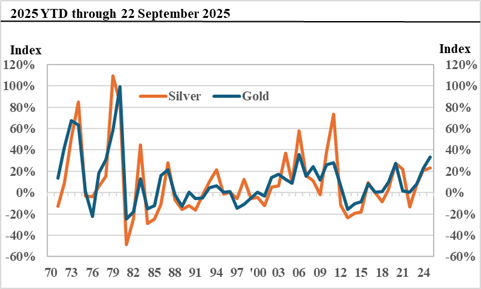

We believe we are in a precious metals bull market. A precious metals bull cycle is led by gold, and silver initially lags. The momentum established by gold then sees the market leadership change from gold metal to the best gold producers, which we are starting to see on the back of the bumper performance of the miners in the June quarter of 2025, and the gold mining stocks are beginning to outperform the yellow metal. At a certain point, silver begins to take over and then powers past gold. What inevitably follows a wonderful gold bull market is a wonderful silver bull market. In a bull market, while the beta is dramatic, the alpha is insane. Jeff Christian of the CPM Group kindly prepared this chart (Exhibit 1) to illustrate how silver prices jump more than gold prices.

Exhibit 1: Percent Change in the Annual Average Gold and Silver Price

Source: CPM Group

For much of the past year, silver appeared to be rangebound in the US$30-35/oz price bracket, but recent weeks saw it move above $40/oz, and as this is written, it has topped $44/oz. Why now? Here is what Michael Steinman, president and CEO of Pan American Silver told us at the Mining Forum Americas in Colorado Springs in September.

“Silver always comes a little bit late to the party, behind gold. We see a lot of demand on the industrial side, about 60%, but to push silver ahead of gold, you also need the investment demand. There is not a lot of silver available for that. There is only about 150Moz available for the investment side, and that has to feed the ETFs, bullion buying, et cetera. But when it comes in, it makes silver run, and that is what we are starting to see now.”

A measure of the relationship and relative value of gold to silver is the gold:silver ratio, which shows the number of ounces of silver you can buy with one ounce of gold. This ratio indicates the relatively overpriced or underpriced nature of the metals relative to each other. Silver may offer more value when the ratio rises, as it has done over the past year. In the 1990s, it averaged about 60:1, but it has been higher in recent years. When the ratio is 80:1, silver is seen as a clear buy over gold, particularly when it starts falling from a peak above 80. This year, the ratio has increased from about 80:1 to 100:1 (see Exhibit 2), which suggests the silver bull has yet to get started. Silver experts expect this ratio to be lower in the future because the silver price will continue to increase rather than because the gold price will come down. Here is what Florian Grummes, MD of Midas Touch Consulting, told us at the Mining Forum Americas.

“Silver is catching up nicely. It has broken out of this long uptrend channel that it has had since the COVID crash, and it is now starting its acceleration phase. … Silver is still extremely undervalued and has a lot of catch-up to do. Silver is coming. We need to be patient. It's still cheap, it's still very undervalued, but it will come.”

Here is what Ronald-Peter Stoeferle, managing partner at Incrementum and publisher of the In Gold We Trust report, told us at the 2025 Precious Metals Summit.

“Silver relative to gold is still extremely undervalued. We are still way above the long-term median as the gold:silver ratio is now at 87-88. The long-term median is around 60, and in a big bull market, it usually doesn't stop at the median, but it ends in extremes. On an absolute basis, silver is also extremely cheap, because it hasn't surpassed the inflation-adjusted all-time highs.”

Exhibit 2: The Gold:Silver Ratio

Source: goldprice.org

A key question is: How sustainable is the silver price rise? Industry participants believe the strong industrial demand for silver will continue to support silver prices going forward. Here is what Mitch Krebs, chair, president, and CEO of Coeur Mining, told us at the Mining Forum Americas.

“The demand fundamentals and demand profile have evolved a lot since 2011. There are end uses now that are a lot more sustainable, with strong growth expected, things like solar panels, and with the AI data centers, we need more electricity, and with that, more silver. These things aren’t going away, and they could help support this price for the longer term.”

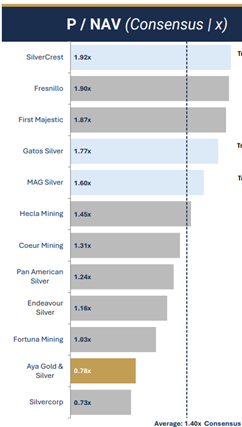

As a precious metals bull starts to run, the precious metals narrative becomes appealing to the generalist investor, which has yet to happen in this precious metals bull market. When the generalists do come, and the leadership changes from gold to silver, there is not enough market cap in the silver space to hold that money, resulting in prices ascending rapidly. What would put the precious metals bull market on steroids would be a major cut in US interest rates, which began in September. With the silver price blowing through $40/oz as September got underway and up 40% year-to-date, some may ask if they missed the silver bull. While some names are more fully valued, several others are yet to catch up, as shown in Exhibit 3.

Exhibit 3: P/NAV of various silver stocks.

Source: Aya Gold & Silver

Silver is a metal that attracts far-flung theories about what makes it go up or down, which a dedicated crowd focuses on rather than the fundamentals that matter. The dual-faceted nature of silver means investors need to be knowledgeable about silver’s drivers to be ready for them when they emerge. These fundamentals were discussed by some of the leading figures in the silver space in the Silver Bootcamp in the Rule Classroom, which, although recorded in February 2023, is still current. We urge you to view this to polish your silver investment game. In the words of Rick Rule…

“Many discussions on silver focus too much on the narrative, which is to say they focus too much on what could happen in the absolutely correct set of circumstances. It's important that you get a rational underlying sense of the market before you get the strategies for how you might take advantage of that market.”

Jeffrey Christian at CPM Group has been analyzing silver for decades, and his fact-based insights cut through much of the distracting narrative that builds around silver. He has identified a couple of myths, such as the world is running out of silver and that silver prices are manipulated. Christian’s Silver Bootcamp presentation is a must-see background for anyone interested in silver.

Some myth-busting facts are that there are 5Boz in refined coins and bars worldwide, of which the banks own 1Boz, which they lease out for interest. Banks are vested in higher silver prices and have no motive for suppressing prices. Also, inventories at rest do not affect the price of silver.

The USGS estimates some 640,000t of silver reserves worldwide, some 22.6Boz. Even with The Silver Institute reporting a supply gap that it believes is growing, the idea that the world is running out of silver is not predicated on geological reality.

Christian said the silver market exhibits some characteristics that appear counterintuitive. When there is a surplus in silver, the price rises, and when there’s a deficit, the price falls. He said this is because surpluses represent periods when investors are bidding up the price of silver. After all, they’re bullish on it, which squeezes fabricators who buy less because of the higher prices resulting in surplus silver. In short, the most significant factors determining silver price trends are macroeconomic, political, and financial, and not the supply and demand aspects of its industrial markets. Here is what Jeffry Christian of CPM Group said in the Silver Bootcamp…

“Investment demand is the kicker, because it's the marginal buyer or seller in silver, and investment demand is determined by trends in investor perceptions of economic conditions, financial market stability, and political uncertainty.”

Although one learns from the past, there are other factors in the current silver market, according to Phil Baker, the former chair of The Silver Institute and former CEO of Hecla Mining. Baker says the current silver market is unlike the failed breakouts of 2011 and 2020 due to the multi-year supply deficit and a profound shift in investor psychology, which sees investors adding silver to their retirement accounts, and heirs, those who inherent silver when a parent dies, no longer liquidating their inherited silver. Here is the former Silver Institute president, Phil Baker…

“In the past, people would put silver into their IRA, and they would be done. Now they're adding to it, and they're continuously adding to it. And what appears to be happening is that heirs are retaining silver, so it has become a long-term generational asset.”

Scarcity

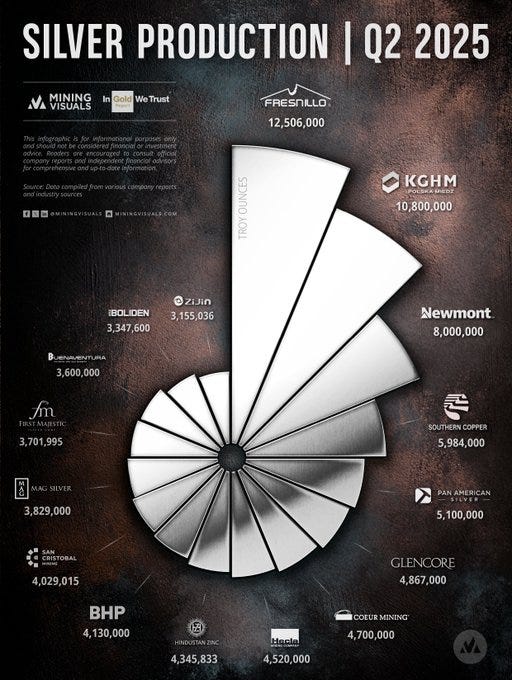

There are relatively few primary silver mines. This also sounds counterintuitive, given the amount of silver reserves that exist, until you read that most silver is produced as a byproduct of gold, copper, nickel, lead or zinc production, as you can see from Exhibit 4. In these operations, silver is not the primary concern of their owners, other than counting as a byproduct credit that lowers the cash cost of producing a pound of copper, for example. This silver essentially has no production cost and will continue to be produced if the principal commodity is profitable. The majority of silver mine supply is therefore price inelastic. Production will not be eased when silver prices fall (the frustrating aspect for silver investors), but conversely, new supply will not come on stream as silver prices increase. The amount of silver mined is linked to the production outlook for the base metals it is produced with. Where this is constrained, the supply of silver will be constrained too.

Exhibit 4: Leading silver producers

Source: Mining Visuals

On the supply side, the world hit peak silver production in 2016, and increasing industrial demand means the silver market is in its fifth year of continuous deficits, with demand of about 1.2Boz, mine supply of 800Moz and 150Moz from recycling.

Scarcity makes good silver deposits, those with grade and scale, very desirable. The past year has seen almost US$5B of silver acquisitions as silver producers seek to load up their portfolios as a silver bull approaches. These were Pan American Silver buying MAG Silver for $2.1B, First Majestic Silver buying Gatos Silver for $970M, and Coeur Mining buying SilverCrest Metals for $1.7B. Coeur is an example of the power silver has to supercharge performance. Having bought Silvercrest, it now has a higher market cap $1B higher than B2Gold, despite producing 500,000oz AuEq compared with B2Gold's 800,000oz.

The relatively few names in the silver space (compared with gold) make silver attractive to investors. Scarcity means that when the investment community becomes interested in silver stocks, there is more inbound investment than there are silver stocks to absorb it, forcing prices higher. It is not uncommon to hear investors state that they have made more money in silver than in gold over the years.

We believe a silver bull market is on its way, so this is a good moment to remind you that a key aspect of investing is timing and having the patience to allow the investment theme to mature. A key point to bear in mind is that you need to look at investment decisions dispassionately and through the lens of what the best opportunity is today to deploy your capital. This can be extremely difficult when many stocks are trading at 52-week highs, as many think they may have missed the boat. Looking at stock charts can be unhelpful for this reason. It is better to look at relative valuations, such as the P/NAV (price to net asset value) multiple, to gauge how well valued your stock of interest is compared with similar companies in its group.

People too often invest according to timeframes they would prefer and not necessarily those required to increase the value of their investments. In a previous silver cycle, Rick financed Pan American Silver at 50c and Silver Standard at 72c, and watched them go to $45 in six or seven years. Staying power can be challenged by the inherent volatility in the silver space. Remember, high beta swings both ways. This volatility can cause people to be shaken out of perfectly good, rational positions. Here is Rick Rule…

“When silver moves, it is a truly spectacular event. You have an asset class that can triple, and that increase can be magnified two or three times in the higher quality equities around that asset class. The rent you get paid is so extraordinary that the holding cost of maintaining a position in anticipation becomes negligible.”

Silver deposit geology

Before discussing specific silver stocks, there are a few notes on things to look out for in their communications. For a silver geology primer, please view the Silver Bootcamp presentation of Brent Cook of Exploration Insights by clicking here, from minute 14:02. Brent provided some pointers to consider when reading silver explorer press releases. Looking for a high grade is an obvious thing, which Brent said is typically +200g/t AgEq. While silver veins can carry splashy grades, Brent advised that such hits must be viewed through the lens of a minimum potential mineable width, which is 1.5-3m depending on vein orientation and mining method. These factors combine, including rock dilution, to produce a mined grade. For example, 1m @ 300g/t over a 3m width gives a mined grade of 100g/t. Dilution costs money and impacts project economics.

We have mentioned that most mined silver is produced as a byproduct of something else. Where silver is the primary metal, it is often accompanied in its deposit by base metals such as lead and zinc, which can complicate metallurgical extraction. Investors need to pay close attention to metallurgical test work, recoveries and what kind of processing is necessary, as polymetallic deposits can be a headache.

Deposit scale is sometimes more important than grade, as you cannot make a big mine from a small deposit. With the metallurgical complexities that silver deposits often have, being acquired is a better exit strategy for most junior explorers than developing a mine. For investors, this means looking for companies with deposits that may appeal to larger companies. A general rule of thumb in the silver space is that a deposit needs to contain at least 100Moz before it gets truly interesting, a quantum of resource that can sustain multi-million ounces of production for a minimum 10-20 years. Here is what Brent Cook of Exploration Insights said in the Rule Silver Bootcamp…

“You don't want a deposit that's not good enough for another mining company to take out. There is a lot of shareholder dilution as a junior gets into the tough part of engineering, metallurgy, and things like that.”

Investing in Silver

There are several ways of obtaining exposure to silver: buying bullion and coins, ETFs, and equities. As the focus of the Rule Investment Newsletter is to talk about stock investing, we will leave buying physical silver aside, other than to note that we recommend that you hold your bars and coins in a secure safe deposit box or vault rather than at home, for its physical safety, and, more importantly, your physical safety. If you don’t need physical silver, you have lower transaction costs by buying products, such as an ETF or the Sprott Physical Silver Trust.

If most silver is produced as a byproduct, can you get exposure to that? The answer is no and yes. There is little to no point investing in a copper company to gain exposure to silver, as the value of a copper company is based on how much copper it produces and how cheaply it does so. While a silver credit reduces its cost base, its share price fluctuates with the vicissitudes of the copper price, not the silver price.

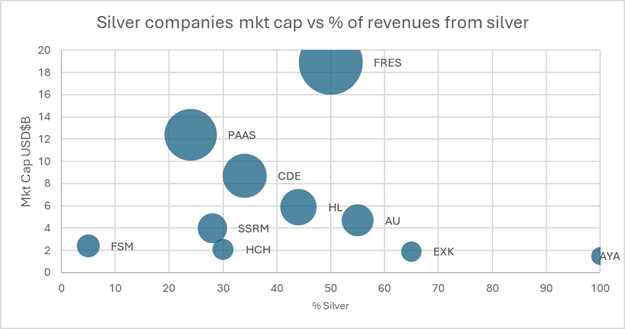

Silver equities enjoy a relative scarcity compared with their gold brethren. One could argue that there are no longer any pure silver producers due to the revenue they generate from gold and base metals, as they have diversified to remain viable businesses (see Exhibit 4). This has seen Silver Standard Resources become SSR Mining and Fortuna Silver become Fortuna Mining, for example, and others should drop silver from their names to reflect their businesses more accurately. However, having silver in a company name still has a certain cachet as it signifies membership of a very select group of companies that can command premium valuations.

Exhibit 4: Percentage of income from silver

Source: RIN from company reports

Maria Smirnova, managing partner of Sprott Inc and senior portfolio manager & chief investment officer of Sprott Asset Management said it is important to track company milestones to hold them accountable to the plans they have shared with the market, and if that is not happening, then cut your losses and move on. See Maria’s Silver Bootcamp presentation here.

“It comes down to math, and what the numbers that the picture you're learning about tell you about the future prospect of the mine. How profitable will the mine be? Is the NPV of the project roughly two times the capital cost. That is a good rule of thumb for me.”

Silver Equities

We will look at three groups of silver equity investments: Latin American producers, hybrid producers and high-quality junior producers or explorers. But first, a word of caution: a precious metal bull market will lift the share prices of all companies, including third-tier silver juniors, which can potentially become value traps for the unwary. There is no sense in being right about the narrative and taking too much risk in stock selection. Rick again…

“The hate that existed three years ago around the silver juniors is completely gone. You are seeing silver explorers that I don't think have a hope of making money at $75/oz complete multi-million-dollar financings to drill off dog deposits.”

Latin American Companies

It is difficult to gain exposure to silver stocks without gaining exposure to Peru and Mexico and the political risk that entails. The silver mining sector is unusual in that it has a large participation from Latin American-based companies that have grown over the decades in the silver mining strongholds of Mexico and Peru.

In Mexico, there is Fresnillo (LSE:FRES) www.fresnilloplc.com and Peñoles (PE&OLES.MX) www.penoles.com.mx/en; in Peru, Buenaventura (NYSE:BVN) www.buenaventura.com/en.

These are Rick Rule-owned

While these companies are listed on Western markets such as the LSE, NYSE and TSX, they expose investors to Latin American political risk, as they are essentially headquartered in Mexico City or Lima, may be listed on local bourses, and often have a large family shareholding and a different business culture.

A couple of examples will illustrate this. Fresnillo is the 56% operating joint venture partner of the Juanicipio silver deposit in Zacatecas, perhaps the best silver deposit in the world today. Yet it let Pan American Silver, an outsider, buy MAG Silver to obtain its 44% stake in the deposit. We don’t know why Fresnillo did not buy MAG, but it could be that it wasn’t prepared to meet or beat the $2.1B offered by Pan American Silver. Pan American, of course, is an attractive partner.

Another Latam company is Hochschild Mining, which is synonymous with silver mining in Bolivia and Peru. It operates the Inmaculada mine in Peru and the San Jose mine in Argentina. Recent developments saw the company venture into rare earths in Brazil and Chile through an investment that is now Aclara Resources (which Paul visited in July). It also bought the Mara Rosa gold deposit in Goias, Brazil, where it has difficulties ramping up to nameplate production capacity.

Through multiple generations of the Benavides family, Buenaventura has held some of the best exploration grounds in Peru for precious and base metals. It has been the partner of choice for some of the greatest mine developments, including Newmont’s Yanacocha and Freeport McMoRan’s Cerro Verde mines. While not a silver company per se, its balance sheet difficulties highlight the challenges of an outsized project portfolio with constant calls for capital.

Hybrid producers

We have used the term hybrid precious metals producers as silver is not the sole product of these companies. The largest, in terms of market capitalization, are Wheaton Precious Metals and Pan American Silver. We will add Rule Symposium participant First Majestic Silver to these.

Wheaton Precious Metals (NYSE:WPM) www.wheatonpm.com

Rick Rule-owned

There is a way to invest in secondary silver production through the company that invented the streaming business, Rule Symposium participant Wheaton Precious Metals, which has bought streams of secondary silver supply from some of the world’s largest base metal mines. We wrote an investment theme on the attraction of royalty & streaming companies in RIN #2, so please refer to that for more on this topic.

Wheaton developed this business from scratch a couple of decades ago. Big miners, such as BHP, Rio Tinto and Glencore, don't care about silver production but need capital. Streaming allows them to generate outside capital at a very attractive price that doesn't dilute their shareholders, and this has become a very attractive source of capital for them. The lack of cost risk makes investing in a streaming company so attractive, as a streamer’s operating and capital costs are fixed. Mining investments are always subject to surprises, such as capital overruns, delays, and cost increases.

The company is on track to produce 600-670,000oz AuEq in 2025, including 20-22.5Moz of silver, about 230,000oz AuEq, or some 39% of revenue going forward. About 83% of Wheaton’s production comes from mines operating in the lowest half of their respective cost curves, which means high margins. Development projects not included in its guidance have the potential of adding ~200,000oz/t AuEq. Here is some more from Randy Smallwood.

“Silver companies were trading at higher market multiples than we were as a gold company, which told me that there was interest in that as a standalone commodity, and that we can probably unlock some value by taking our non-core byproduct, silver, and putting it into a vehicle that silver investors can focus on.”

Pan American Silver (NYSE:PAAS) www.panamericansilver.com

Rick Rule-owned

Pan American has been in the headlines for its $2.1B acquisition of MAG Silver. The addition of the 44% of Juanicipio will add 6.5-7.3Moz of annual production at an AISC of $6-8/oz. This will add an estimated $98M to pro-forma free cash flow in 2025, while its free cash flow is expected to grow 23% over the next three years. It will also lower the company’s overall production costs.

The company produced about 5.1Moz of silver and 179,000oz of gold in 2Q25. Its share price is up 80% year-over-year as its market capitalization has grown to $15.5B. Its cash balance topped $1B, with $233M in free cash flow. The company increased its dividend by 20%, and its dividend policy means dividends increase when its net cash increases.

The company has 10 producing silver and gold operations with reserves of 468Moz silver and 6.7Moz gold, with growth potential at La Colorada Skarn in Mexico, where it sees decades of future production; Escobal in Guatemala and Navidad in Argentina, although these latter two do not currently have a clear line of sight into production for social reasons. The forecast production this year is 20- 21Moz of silver and 735,000-800,000oz of gold. Panam has also sold several non-core assets in recent years and raised $990 million while retaining six royalties.

First Majestic Silver (NYSE:AG) www.firstmajestic.com

First Majestic Silver stubbed its toe when it deviated from its motto of one metal, one country when it bought the Jerrit Canyon gold operation in Nevada for far too much money (US$470 million) in 2021. The challenges this operation presented subsequently saw the company return to its roots of silver in Mexico when it bought Gatos Silver to bolster its Mexico portfolio by adding the Los Gatos mine to its San Dimas and Santa Elena operations. Jerrit Canyon aside, First Majestic has a knack for acquiring unloved assets, recapitalizing them, and getting them to work. The Los Gatos acquisition will continue if the company successfully extends its reserve life.

A positive from First Majestic’s foray into the US is its creation of a mint in Las Vegas, where it can produce its own silver coins and bars, and intends to send an increasing amount of the silver it produces for refining. A primary reason is that cutting out the middleman (third-party refiners) enables First Majestic to make more money from each ounce it produces. It also provides First Majestic with a marketing bonus in that it can strike coins and bars bearing the company’s logo, where other silver producers pay third-party refiners to obtain them.

One of First Majestic’s greatest assets is its CEO, Keith Neumeyer, and the marketing leverage he has at his command. Neumeyer is a passionate and opinionated advocate for the silver sector and one of its most recognizable faces. It would be overreaching to say that Neumeyer can move the silver price, even if he forecasts a triple-digit price, but his timely comments on silver can move First Majestic’s share price. Click here for Rick’s pre-Symposium video with First Majestic Silver.

Other hybrids of note are Coeur Mining and Hecla Mining, companies with a centennial tradition as US silver producers, and the brand awareness and experience that goes with this. Not all this experience has been pleasant, as both companies have had a chequered track record of capital allocation in recent decades. While this does not take away from their leverage to silver, they will not be discussed further here.

First Majestic was a 2025 Rule Symposium participant. Click here for Rick’s interview with CEO Keith Neumeyer.

High-quality juniors

We think a few high-quality junior producers and developers will perform well in a silver bull market, some of whom are Rule Symposium participants: Vizsla Silver, Abra Silver, Aya Gold & Silver and Dolly Varden Silver.

Vizsla Silver (TSX:VZLA) www.vizslasilvercorp.com

Rick Rule-owned

Vizsla Silver aims to have a financing plan in place later this year for the development of its Panuco silver project in Sinaloa, Mexico, as it waits for the receipt of an environmental permit for the project, with the company to raise about $200M for the $224Mmillion capex. Vizsla aims to produce 15Moz/y AgEq for 11 years, including 9Moz/y Ag at an all-in sustaining cost of $8/oz, from the second semester of 2027. It is developing a decline to undertake a permitted test mining program that will see it take a bulk sample. Panuco hosts a January 2025 measured and indicated resource of 12.96Mt grading 307g/t Ag, 2.49g/t Au, 0.27% Pb & 0.85% Zn containing 222.4Moz AgEq, with another 138.7Moz in inferred resources based on 373,000m of drilling. The company has $100 million in cash and could sell its 17% stake in Vizsla Royalties, which is valued at about $25 million. The company has a market capitalization of C$1.3 billion.

Paul visited Panuco in October 2022, drawn by flashy drill results, many of which have contained intervals of more than 1kg of silver equivalent, and a drilling program that has racked up hundreds of thousands of meters to define the Copala and Napoleon structures. The veins have scale. Napoleon, for instance, is an epithermal vein with intermediate sulfidation, with an average width of 3.5m over a 2.5km strike length, vertical extent of 550m, and base metals concentrations. The project also includes a 500tpd mill, 35km of underground mine workings, tailings facilities, a paved highway and powerlines which pass through the property. A feasibility study is expected later this year, while drilling targets other veins on the Panuco property.

Key catalysts in the next 12 months include the results of a 25,000t bulk sample from Copala and Napoleon to confirm metallurgical test work and the mining method, the results of an optimized metallurgy program to confirm the flowsheet, a feasibility study before year's end, and ongoing discovery potential.

Abra Silver (TSX:ABRA) www.abrasilver.com

Rick Rule-owned

AbraSilver Resource is exploring the Diablillos project in Salta, Argentina, and updated its measured and indicated resource in July to 104Mt @ 59g/t Ag & 0.51g/t Au, containing 199Moz silver and 1.72Moz gold, or 350Moz AgEq across five deposits at Oculto, JAC, Fantasma, Laderas and Sombra. Within this are a tank leach resource of 73Mt @ 79g/t silver & 0.66g/t gold, containing 186Moz silver and 1.55Moz gold, and a heap leach resource that adds 31Mt @ 13g/t silver & 0.16g/t gold. Abra intends to complete a feasibility study in the March quarter of 2026.

Diablillos is one of the lowest-grade deposits we feature in this investment theme, and that is because it has the scale to be a successful mine, maybe as high as 13Moz/y, which would make it one of the biggest producers worldwide. A December 2024, PFS detailed a 9,000tpd operation with an initial capital expenditure of $544M, with an average recovery rate of 85.2% and an AISC of $12.67/oz AgEq, which it says is below the $19.58/oz average of existing producers. The project is in the heart of Salta’s mining district and is surrounded by infrastructure. The project is surrounded by lithium, silver and copper mines and development projects, which means there are roads, powerlines, and water on hand that the company will not have to pay to develop. Abra is undertaking a 20,000m phase V drilling campaign with Oculto East, which is more gold-rich than the JAC zone, becoming a priority.

Key catalysts in the next 12 months include obtaining an environmental permit, being accepted into the RIGI large infrastructure investment project special financial regime, and completing a feasibility study. Click here for Rick’s pre-Symposium video with Abra Silver.

Aya Gold & Silver (TSX:AYA) www.ayagoldsilver.com

Rick Rule-owned

Aya is the purest silver play of the companies featured in this report, with 100% of its metal coming from silver. The company produced 2.1Moz in the first half of 2025 from the Zgounder mine, with an average processed grade of 170-200g/t and 84-88% recovery. It hosts M&I resources of 96Moz @ 306g/t Ag. The company also has development upside through its Boumadine gold, silver, lead & zinc deposit that hosts 74Moz AgEq of indicated resources @ 448g/t AgEq and another 377Moz of inferred resources. Zgounder has grade and has provided some of the top 50 global silver intersections in recent years, including 21.6m @ 3,956g/t Ag. The company has guided the production of up to 5.3Moz this year at an AISC of up to $17.50/oz. Key catalysts in the next 12 months include Boumadine metallurgy and PEA.

First Majestic was a 2025 Rule Symposium participant. Click here for Rick’s interview with CEO Benoit La Salle.

Dolly Varden Silver (NYSE-A:DVS) www.dollyvardensilver.com

Dolly Varden has been one of the most exciting silver exploration stories over the past two years, not only because of its high-grade results at its Kitsault Valley project and investment from Eric Sprott and Hecla Mining, but also because it is the only silver exploration company in the Golden Triangle of British Columbia, Canada. It has been drilling two main target areas called Homestake and Wolf. Kitsault is a structurally hosted gold-silver deposit, which was mined in the past, with an estimated 20Moz of silver produced in the 1950s. The project has two halves: the silver-rich Dolly Varden-Torbit area, including Wolf, to the east and the gold-rich Homestake area to the west. With Wolf and Torbrit trending towards each other, it has been hypothesized that the two may connect, which would be big news.

Dolly has an indicated resource base of 34.7Moz of silver and 166,000oz of gold and 29.3Moz of silver and 817,000oz of gold in the inferred category. There is also copper, zinc and lead. At 64Moz of silver, Kitsault is shy of the magic number, but with 55,000m drilling program underway, that number is expected to continue rising.

Kitsault is virtually surrounded by Hecla Mining, which picked up adjacent ground in 2016 and has tried to buy Dolly's predecessors. Hecla owns 15% of Dolly and has participated in several financings. Hecla also has the right of first refusal if someone else makes a bid for the company. The Golden Triangle is not as remote as it once was, with Kitsault benefiting from a 25km road maintained by the operators of a tidewater port, 30km from a powerline and 46km from a deepwater port. Dolly also listed on the NYSE-American in April 2025. Click here for Rick’s pre-Symposium video with Dolly Varden Silver.

Silvercorp Metals (TSX:SVM) www.silvercorpmetals.com

It is a company with which Rick has a long history, having helped take it public in 1991 under its original name of Spokane Resources. The name change occurred in 2005. The company specializes in mining high-grade narrow veins, with operations in China and development projects in Latin America.

A quick note that it is difficult to prove up enough reserves in high-grade narrow vein deposits to provide long mine lives, as companies cannot afford to do enough delineation drilling to have more than five or six years ahead of them. It is common for such mines to have had two to five years of mine life ahead of them for 10-20 years! This makes it difficult to value them as you cannot see very far into their potential future. This is a factor in the Las Chispas mine that Coeur obtained when it bought SilverCrest.

Such deposits can also be challenging to measure accurately, as changes in the assumptions used can have dramatic impacts. A 2023 technical report detailed fewer reserves than anticipated by the market due to narrower and more widely dispersed veins than initially modelled, with higher operating costs leading to a higher cut-off grade. Gatos Silver suffered a similar experience at its Cerro Los Gatos mine in 2022, which was attributed to material errors in the original geological modelling. Neither of these instances inhibited transactions on what continued to be exceptional assets.

Silvercorp is led by chair & CEO Dr Rui Feng, who also founded New Pacific Metals. Again, there is a halo of political risk as Silvercorp operates mines in China, and its growth pipeline is in Ecuador, where it bought the El Domo and Condor projects through the C$200M acquisition of Adventus Metals in 2024. Silvercorp’s timing could prove to be shrewd both in buying just before a gold and silver bull market gets underway, as well as in Ecuador, which elected a pro-mining president with Daniel Noboa.

New Pacific Metals (TSX:NUAG) www.newpacificmetals.com

New Pacific is in a similar position in Bolivia. Bolivia was once a formidable silver producer, and perhaps the most significant deposit the world has ever known, Cerro Rico, features on its flag. It is still a sizeable silver producer at 48Moz in 2024, mainly from the San Cristobal, San Vicente and San Bartolome mines.

Political risk has largely seen Bolivia fall from the mining and exploration map over the past 20 years during the multiple presidencies of the MAS party, initially under President Evo Morales, and later his successors, such as Luis Arce. MAS is no more, however, as the first round of the August presidential election saw MAS kicked aside due to a lack of economic and social progress; the MAS regime came to be seen as increasingly corrupt and self-serving. MAS was dumped out in the first round after polling just over 3% of the vote. This leaves Bolivia ready to elect its first non-left president for over two decades during the second round run-off on October 19 between senator Rodrigo Paz and former president Jorge Quiroga. Both will want to promote mining to boost the economy, create jobs and pay for public services.

Paul visited New Pacific’s Silver Sand project in Potosi in 2019 and saw the high-grade vein potential for himself. Silver Sand has a 2024 PFS and has been stalled in permitting for years, and could potentially progress under the next government. It aims to produce 12Moz/y of silver for 13 years at an AISC of $10.69/oz, following an initial capital investment of $358M. The company aims to produce another 6.6Moz/y for 16 years from its Carangas deposit in Oruro, following an investment of $324 million. If both deposits come into production, New Pacific’s potential annual silver production would be second only to Pan American’s. The company would be one of the first to benefit from a change in direction of the political winds in Bolivia.

Outcrop Silver & Gold (TSXV:OCG) www.outcropsilver.com

Outcrop Silver & Gold's Santa Ana project in Tolima, Colombia, is one of the highest-grade primary silver deposits in the world, and is in a historical mining district producing precious metals for at least 500 years. Santa Ana is located near Falan, part of the Mariquita District, and has a long mining history dating back to 1585, with historical grades at the Frias Mine on the south-central part of the project of 1.3kg/t. Santa Ana hosts mesothermal and epithermal quartz veins containing carbonates containing sphalerite, galena, pyrite and silver sulfosalts in vein structures that can run for over 2km with high-grade silver-gold shoots.

Paul visited Santa Ana in December 2024 and could see why Eric Sprott invested in the company three times to obtain a 20.6% holding. The resource is currently modest at 24.2Moz AgEq at a 614g/t silver equivalent, with another 13.5Moz in inferred from seven veins. Several other veins have been defined with a resource update in early 2026. The mineralogy comprises the silver sulfides mineral argentite (88%), sulfosalts (9%), and electrum (3%), it has the benefit of floating well. Metallurgical test work has recovered 96.3% for silver and 98.5% for gold.

Mining narrow veins can be done profitably, particularly when the grades are like Santa Ana's. Diluting the veins over a minimum mining width of 1.2m still results in a mine grade of over 500g/t. The question is, are there enough high-grade veins with which to form a mining plan? Outcrop has defined 37.5Moz in seven veins through 40,000m of drilling, so with each vein hosting about 5Moz, the company needs to find 20 veins to get to the 100Moz figure, and it has 37 targets. The geological structural control sees the veins run consistently in the horizontal plane with little deviation, which enables company geologists to define a vein with relatively few drill holes and relatively generous drill spacing. Drill spacing can be 80m for inferred resources and 60m for indicated, so it can confirm a target with six to nine drill holes. The company also sees veins coming every 200m along strike and parallel veins 300-400m away. Some 24,000m of drilling are planned for 2025 to update the resource estimate in early 2026. Here is what company president & CEO, Ian Harris, has to say.

“We don't like taking risks. We know exactly which veins are going to produce the ounces for us, how much they cost per meter, how many ounces we get per meter, and we are trying to get those ounces as cheaply as possible. For every dollar I spend, I could create $4 in value. If we can get 100Moz, we are looking at the production of 7-10Moz/y and being one of the 20th largest silver producers in the world.”

Highlander Silver (TSX:HSLV) www.highlandersilver.com

Highlander Silver is drilling the San Luis high-grade epithermal silver vein project in Ancash, Peru, which it obtained from SSR Mining. Some of the biggest names in the business have taken positions in the company, including Richard Warke and the Augusta group, the Lundin family, and Eric Sprott, who, together with management, hold more than 65% of all the issued and outstanding shares. SSR put together a measured and indicated resource of 348,000oz of gold @ 22.4g/t and 9Moz of silver @ 578.1g/t. SSR also advanced an economic study and environmental impact statement before the bear market bit in 2012, and it pivoted towards the Marigold gold mine in Nevada, US, and other acquisitions. That resource is on one vein called Ayelen, and Highlander has discovered several more across its 230km² property. Its initial drilling targeted the Bonita vein, which has a 700–800m strike with individual structures up to 30m wide, multiple times wider than what is seen at Ayelen.

Discovery Silver (TSX:DSV) www.discoverysilver.com

Rick Rule-owned

Discovery Silver has been one of the most prominent development stories for several years, with its Cordero project in Chihuahua, Mexico, but while the company is about ready to mine the project, permitting has taken its sweet time. Paul visited Cordero in October 2022, and while he saw it is in a remote part of Chihuahua, away from any communities, the political climate in Mexico today may not be conducive for building an open pit operation, even though Chihuahua already has two open pit mines: Pan American Silver's Dolores and Pinos Altos of Agnico Eagle Mines. Water is a contentious issue in Mexico and Chihuahua is a desert state. The company filed it environmental permit application in August 2023.

A February 2024 feasibility study for Cordero detailed the production of a whopping 33Moz/y silver equivalent at an AISC of $13.47/oz for 19 years. That is about twice the size of the next biggest silver mine in the world. The $606M first phase would be a 26,000tpd operation, with an expansion in year three to 51,000tpd to exploit reserves of 327Mt @ 29g/t silver, 0.08g/t gold, 0.41% lead and 0.72% zinc, containing 302Moz silver, 840,000oz gold, 2.96Blb lead and 5.18Blb zinc. The company estimates metallurgical recoveries of 87% for silver, 18% for gold, 89% for lead and 88% for zinc.

Discovery pulled a rabbit out of the hat by purchasing the Porcupine mine in Ontario, Canada, from Newmont in April 2025 for a relatively modest US$425M. Discovery CEO Tony Makuch has decades of experience operating in Ontario, and is looking for upside potential. Becoming a producer overnight gave a shot of adrenaline to the company’s share price, and Porcupine’s cash generation has taken the pressure off getting the Cordero permit for the company. Discovery is now a gold miner with a large silver development project with the time and patience to get permitted. This can be seen with Cordero being relegated to slide 22 of its 23-slide August 2025 deck, which perhaps says more than words can about the turn in company focus. However, Cordero continues to give Discovery leverage to the silver price. Its key catalyst is getting its Cordero permit.

Blackrock Silver (TSXV:BRC) www. blackrocksilver.com

Finally, we will look at one of the only US opportunities in the junior space, with its Tonopah West project in Nevada. Historical mining from this project area is why Nevada is known as the Silver State.

In September 2025, it published its first indicated resource of 1.33Mt @ 493g/t AgEq for 21.1Moz and 5.14Mt @ 525.9g/t for 86.88Moz in inferred resources, for an aggregate of 108Moz. This was essentially the same number of ounces as its 2024 resource, which the market did not like and saw the company sell down 10-15%. The company poorly communicated that it was a resource focused on upgrading the quality of the resource at Tonopah West, and that Blackrock intended to release another resource update soon, showing expansion. Here is CEO Andrew Pollard.

“The biggest question mark over our project since we made our discovery five years ago, and as we have materially grown the size and scale of it, is that people didn't believe our ounces were as good as they looked."

A 2024 preliminary economic assessment (PEA) outlined production of 4-5Moz/y of silver and 54,000oz/y of gold, or 8.6Moz of silver equivalent for 7.8 years from a 1500tpd conventional underground mining operation. The head grade is 55% higher than that of the next closest silver developer in the world. The resource update improves confidence in the first two to three years of production. The second resource update aims to increase the mine life to 10 to 12 years.