The Coppertunity

Rule Investment Newsletter #12

In 2025, copper became a critical mineral in the US due to its importance in the electrification of everything. Copper is the next bull market, with a great risk/reward setup, as supply is declining in a market already in a structural deficit. In this edition of RIN, we explore why copper has a bright future. As Rick says:

“The copper price has a coiled spring aspect to it.”

Copper will be a key theme at the 2026 Rule Symposium in Boca Raton, Florida, from July 6 to 10, 2026. The event will feature new participating copper companies, including Ivanhoe Mines, Arizona Sonoran Copper Company, Amerigo Resources, McEwen Copper, Aldebaran Resources, Hot Chili, and Mundoro Capital. To register, click the button below.

Rick and I will participate in a live Q&A about RIN #11 Who the wolf, who the sheep in Latin America? at 14:30 Eastern time on Thursday 19 February. Click the following link to participate in that: https://streamyard.com/watch/tirCsDDVRJwJ

Now, back to Copper.

First, a bit of my background in copper: from 2023 to 2008 I lived in copper capital Santiago, Chile, where I was a copper reporter for Metal Bulletin (Now FastMarkets). This was during the supercycle, a situation similar today, in which the copper price ran to record levels and the market was very twitchy about the supply-demand balance. Towards the end of that period, I was also a consultant for the leading copper consulting group CRU. Over the years, I have visited many copper mines and projects in Chile, Argentina, Bolivia, Peru, Ecuador and Colombia, Arizona and Alaska, and I also make an annual pilgrimage to Santiago to attend CRU’s World Copper Congress, which is where you will find me come April.

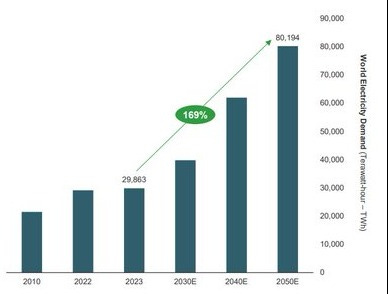

Why all the fuss about copper? Copper is a key energy transition material due to its superior electrical conductivity, which builds on its role as a vital industrial and construction material. Take a look at these to charts: the International Energy Association (IEA) estimates world electricity demand will increase by 169% by 2050.

Exhibit 1: Forecast electricity demand

Source: IEA

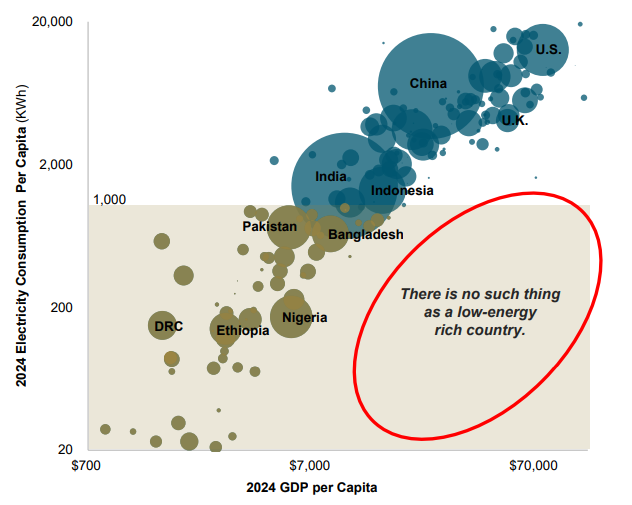

Why? Because countries are getting richer in terms of GDP per capita, and that translates directly into greater energy consumption. There is no such thing as a low-energy rich country.

Exhibit 1: ElectElectricitygricity & Income Per Capita

We could end this RIN here, because the above is the main driver you need to be aware of for the copper investment thesis, but of course, we will enter into the details of why this matters. In the words of entrepreneur, Frank Giustra:

“What we’re facing with copper right now feels different than a boom—deeper, more structural, more consequential. This is more than a commodity rally driven by speculation or short-term supply hiccups. It’s the early stages of a secular bull market that could last a decade or more, as demand grows and supply struggles to keep pace. The world is waking up to a crunch that’s been building for years.”

Along with steel and aluminum, copper is one of the industrial metals that is required for everything. No copper: no life. Sometimes literally, as copper is also a biocide that kills or inhibits the growth of harmful microorganisms. Why are we focusing this RIN on copper? With the copper price increasing by about 34% in 2025, hitting record pricing levels above $6/lb or $13,000/t as 2026 got underway, and an outlook for market deficit inspired higher prices in the future, it is a good time to be in copper. Here is Rick:

“In the global economy, you’re seeing supply decreases being met by demand decreases, and so the price is improving, but the shortfalls in copper become acute five years from now, and acute is a much more aggressive word than serious or concerning. Acute means it becomes a problem for humankind. That is where we’re headed in the copper space.”

Copper is a cyclical market. Currently, it is trending towards a high point, driven by increasing demand from energy transition applications, data centres, war materiel, and general economic growth. Tight supply has pushed the copper price over $12,000/t. Why are copper prices riding high? Here is the Chile consulting group, GEM:

“This upward [price] movement reflects a combination of monetary, geopolitical, and structural factors, notably the recent decision by the US Federal Reserve, signals from China’s economic policy outlook for the coming year, and the particular configuration of inventories across the world’s main metal exchanges.”

OK, but what does that mean? In short, a tight supply situation is becoming even tighter, and geopolitical factors are intensifying its impacts and implications.

In addition to normal GDP growth of 2-3% pa, copper demand is boosted by energy transition applications, data centers, and increased military spending. Demand from China remains robust and India is working hard to join the electrification and industrialization party. Additionally, the US looks likely to receive a nuclear power boost, which could lead to possible grid upgrades that the country has not seen in more than 20 years. With a rising population and rising temperatures, the demand for power-hungry air conditioning will also increase. Here is S&P Global in its January 2026 paper Copper in the Age of AI: The Challenges of Electrification:

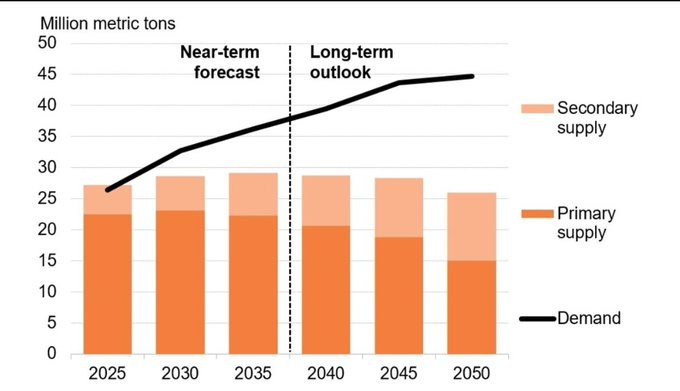

A looming copper supply gap is poised to widen as electricity demand accelerates and new vectors—such as the race for artificial intelligence and surging defense spending—add to the call on copper.

Exhibit 1: Forecast copper supply deficit

Source: Bloomberg NEF

Total demand for copper in 2023 was 26-27Mt, about one quarter linked to clean technologies. Demand is expected to grow by ~40% to 2040 to 42Mt, with clean technologies increasing proportion to 45% of the total according to the International Energy Agency. With S&P forecasting a production peak of 33Mt in 2030, the industry forecasts a supply gap of almost 10Mtpa opening by the end of the decade, or 20-40% of current world supply. Wood Mackenzie forecasts global demand will surge by 24% by 2035, rising by 8.2Mtpy to 42.7Mtpy. In December 2025, BloombergNEF’s reported in its Transition Metals Outlook 2025 rising demand for some critical metals, including copper, is outpacing supply chain capacity, creating structural market imbalances (see Exhibit 1). Leading diversified miner BHP (LSE:BHP) suggests demand will rise 70% to more than 52.5Mtpa by 2050, driven by urbanization, electric vehicles and renewables, with the need to inject US$250B on copper supply alone. BNEF said:

“Copper faces significant pressure, with the market entering a structural deficit next year and facing a projected shortfall of 19Mt by 2050 if new mines and recycling facilities are not developed.”

The lowering of US interest rates adds to this as a lower cost of capital helps industry, construction and the property market, which are all big copper consumers. China accounts for about 58% of global demand, and its latest five-year plan sees higher investment in electrification, power grids, renewable energy, electric transportation, and digital infrastructure, all copper-intensive sectors. The International Copper Study Group (ICSG) projects that global refined copper consumption will grow by around 2.1% in 2026, with the global refined copper market to shift to a deficit of about 150,000t in 2026.

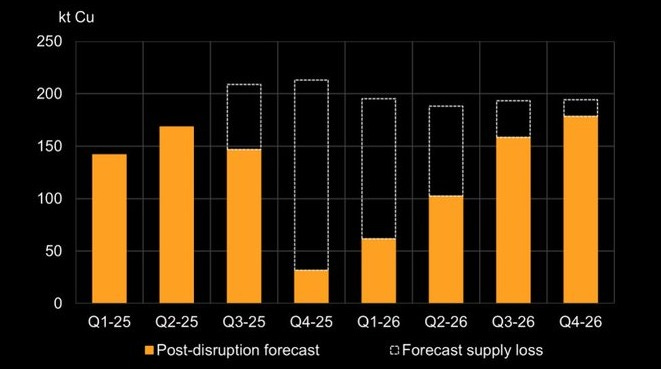

Exhibit 2: Grasberg mine quarterly copper output

Source: Benchmark, Freeport McMoRan

This outlook is colored by output reductions at major mines. In any given year, there are production outages of 0-5% of total capacity. In 2025, more than 3% of global copper supply is currently offline or facing production issues. These include outages at Freeport McMoRan’s (NYSE:FCX) Grasberg mine in Papua New Guinea (see Exhibit 2), Ivanhoe Mines (TSX:IVN)’ Kamoa-Kakula in Democratic Republic of Congo and First Quantum Minerals’ (TSX:FM) Cobre Panama in Panama. Codelco’s El Teniente and Teck Resources (TSX:TECK) Quebrada Blanca in Chile also face production issues. Here is what BHP CEO Mike Henry told CNBC:

“All it took was a few disruptions at a few copper mines around the world to all of a sudden send the market into deficit, and to see copper prices reach record highs. We’re expecting that between now and the end of the decade, that crunch is only going to get tighter.”

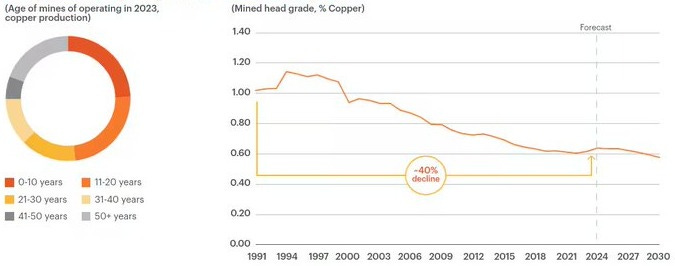

Exhibit 3: Copper mines aging, grade declining

Source: S&P Global Market Intelligence

These short-term issues grab the headlines, but a longer, more powerful trend is at work, as more than half of copper production comes from mines that are over twenty years old, and average ore grades have declined by about 40% since 1991 (see Exhibit 3). This will continue into the future, with about half of global production facing additional grade decline over the next decade. Declining grades increase the cost of doing business, as companies need to extract more rock to produce the same amount of copper, leading to higher energy consumption and higher costs. The cost to produce the marginal tonne of copper is increasing, and therefore, underlying copper prices will continue to rise.

The cyclical nature of the copper market means its price can drop precipitously too. The Supercycle of the early 2000s saw the copper price reach $4.50/lb, driven by the rapid growth of the Chinese economy. However, it came to an abrupt halt with the 2008 global financial crisis, which led to a significant decline in the copper price, retrenching below $2/lb. It is the fear that this situation will repeat or that the cycle will run its course that keeps copper executives awake at night and restrains them from making new investments. More about that later. In the words of Rick:

“The cure for high prices is high prices.”

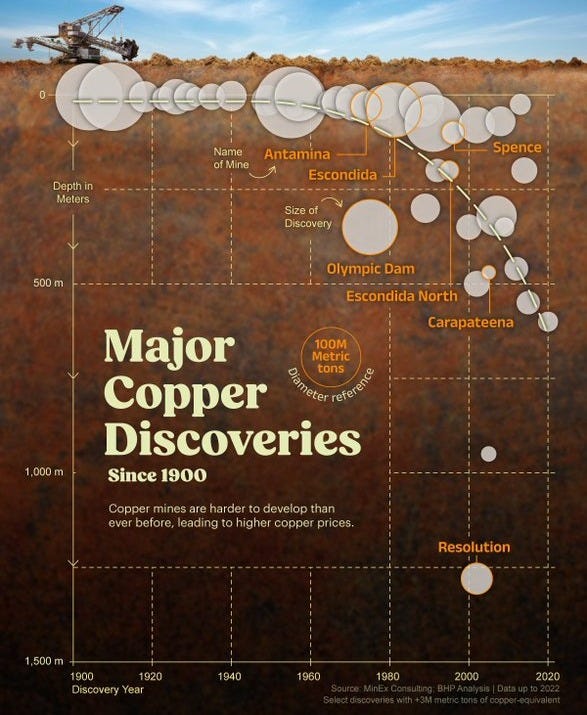

Exhibit 4: Major copper discoveries

Source: Visual Capitalist from BHP

Supply response

With high prices and a looming deficit, many people, including governments, question why the copper sector is not expanding its capacity. There are several reasons for this: a lack of new discoveries (see Exhibit 4), new discoveries are smaller and lower grade than in the past, and deeper, which makes them more difficult and expansive to develop.

Another factor is risk/reward, in that few boards and CEOs in the sector see the rewards being commensurate with the risks. The cyclical nature of the market means that poor timing on project acquisitions and developments can be fatal, as prices tend to crash when there is too much supply for the market to absorb. We can add that projects take longer to explore and obtain permits, development costs continue to increase, and deeper builds take years to complete, often overlapping with political cycles. Consider this: many projects are profitable at $4/lb but they are not being built at $5.50/lb. Why? The answer is that there is risk everywhere and in everything, and the economics have to be attractive enough to take that risk. Here is what BHP CEO Mike Henry told CNBC:

“We expect [demand’s] going to be up by 70% between now and 2050, but supply is becoming more and more difficult to bring on. Fewer mines are being found. The mines that are being found are oftentimes smaller, lower grade in tougher jurisdictions, and so it’s hard to bring those mines on quickly.”

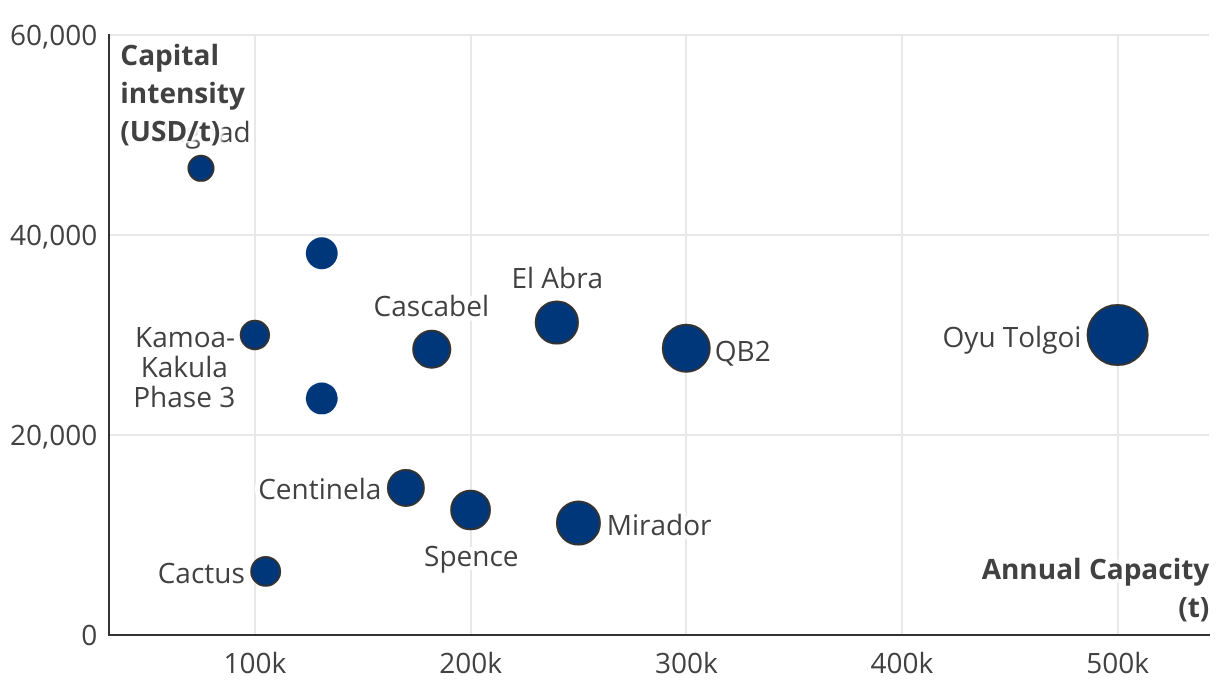

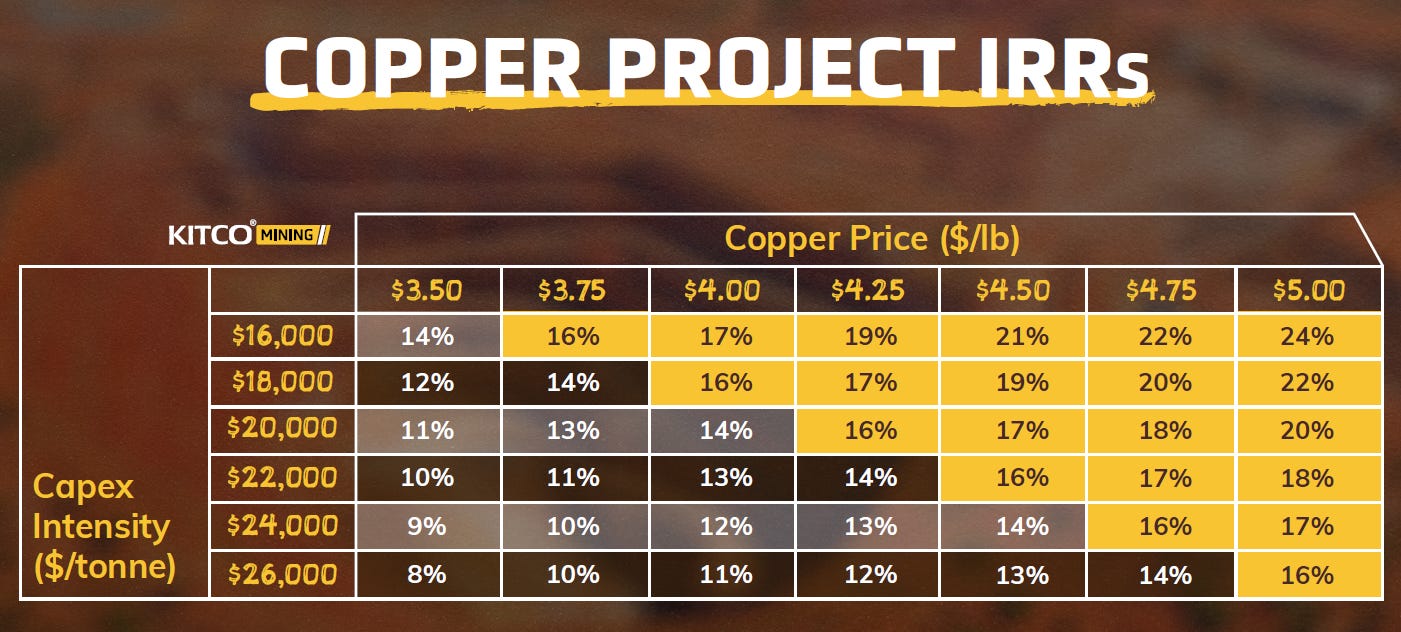

Exhibit 4: Copper project capital intensity

Source: Company reports

Projects are getting more expensive to build. The smallest projects will cost $1B, medium-sized projects $3-5B, and bigger projects $5-10B. The capital intensity of projects is increasing: that is, the cost to build one tonne of production capacity. This is moving towards $20,000/t (see Exhibit 4), which acts as a brake on development as it increases financial risk, particularly given the possibility (likelihood) of cost overruns. No one wants to repeat the experience of Teck Resources and its QB2 development in Chile where project costs doubled after ground was broken.

A high metals price environment does provide new options for miners. BHP just raised $4.6B from Wheaton Precious Metals for a silver stream on its 33.5% stake in the Antamina Cu mine in Peru. An almost indentical deal in 2015 saw Glencore raise $900M.

Exhibit 5: Copper project IRR, Copper Price and Capital Intensity

Source: Solaris Resources, Kitco Mining

Most companies require projects to exceed a 15% IRR for them to be investible. Solaris Resources created a matrix of the sensitivity of IRR to the copper price and capital intensity (see Exhibit 5), which shows way a $5.50/lb copper price does not incentivize new mine building: lack of profitability.

Declining grades mean that project throughputs are becoming larger to generate the economies of scale necessary for them to be economic. This is why Robert Friedland, founder and executive co-chair of Ivanhoe Mines, talks of the industry’s “Herculean task” of filling the supply gap. He said:

“This deficit is going to have to be adjudicated by price. The price goes higher, and it has to stay much higher and for a very long time before you can stimulate the construction of low-grade porphyry copper projects.”

In addition to cost, this is also pushing the technical boundaries of what is possible. This is most clearly seen in brownfield expansions at leading mines, which are jumping from massive to mind-boggling throughputs. Freeport-McMoRan is looking to expand its El Abra copper mine in Chile—a joint venture with Codelco—that would supercharge the mine from the 98,400t it produced in 2023 to 340,000tpy (and more than 4,100tpy of molybdenum) by expanding throughput from 125,000tpd towards 400,000tpd. Also in Chile, Antofagasta (LSE:ANTO) will invest $4.4B on a new concentrator at its Centinela mine to add an initial 95,000tpd of capacity to the existing 105,000tpd, with a second phase to increase the expansion to 150,000tpd possible. You can build the biggest SAG (semi-autogenous grinding) mill in the world, but what if it doesn’t work as planned? Here is David Strang, executive chair of Ero Copper (NYSE:ERO):

“42-ft SAG mills are a bespoke bit of equipment. The end plates must be poured in one piece, and only two or three companies in the world can make them, and they cannot make that many each year.”

Despite the risks, copper producers have favored brownfield expansions, because they know the deposits and metallurgy, they have established infrastructure, and often only require permit extensions or expansions. Greenfield projects, by comparison, present a litany of uncertainties and challenges, leading to very long development times.

The high levels of risk in the inherent business is why copper miners call for stable fiscal and regulatory environments. On that front, 2025 has been a year of disruption, sowing uncertainty and causing the sector to wait and see how things look when the dust settles before making multi-decade investment decisions. Coup attempts in Africa and regimes like Mali that seek greater government control make miners nervous. Latin America is in the midst of a presidential election cycle, with changes in government in Chile, Peru, Bolivia, Mexico, Ecuador, and Colombia occurring within two years, with far-reaching ripples. We discussed this in RIN #11.

Copper has long been a strategic metal for Chile and Peru, where its development has been economically and socially transformational. It could be for Colombia, Argentina and Panama too, but it large copper mine developments often become politicized, a risk that overhangs projects, such as Tia Maria (Peru), Quebradona (Colombia) and Cobre Panama (Panama). We aim to talk about the changing political landscape in Latin America in a future issue of RIN. Let’s look at some of those disruptions.

Trump

The US had 25 copper mines, two smelters, and two primary refineries in 2024. It consumed over 1.6Mt of refined copper, with just under half imported. Domestic refined copper production was 880,880t in 2024, which is projected to rise to 1.2 Mt by 2026. Processing capacity remains a key bottleneck, with 30% of mined output exported as concentrate. In the global copper market, the US is a relatively small consumer, but that does not mean it cannot be a disruptive force.

President Trump wants more copper produced in the US to reshore industrial capacity and create jobs. Beyond this, he understands the critical and strategic role it increasingly plays in the electrified and digital world, as well as in weapon systems. No copper supplies reduce a nation’s ability to conduct war. To this end, Trump wants the US to export fewer copper concentrates and copper scrap, particularly to geopolitical rival China, which dominates copper smelting. Incidentally, Benchmark Minerals Intelligence estimates a copper concentrate deficit of 1.1Mt in 2025 and forecasts it to increase to 2.6Mt in 2026.

President Trump initiated a Section 232 investigation under the 1962 Trade Expansion Act in early 2025 to assess whether copper imports pose a national security threat. The threat of tariffs on copper led to a significant premium emerging between copper prices on the New York futures exchange (COMEX) and the London Metal Exchange (LME) as US importers accelerated their purchases. US copper inventory rose to more than 400,000t, while LME stocks fell to less than 100,000t. Upon the conclusion of the study, President Trump imposed 50% import tariffs on semi-finished copper products, such as tubes and wire, in July 2025, surprising the market by steering clear of primary copper imports (cathode and concentrate). The White House said:

“The [Commerce] Secretary found that the present quantities of copper imports and the circumstances of global excess capacity for producing copper are weakening our economy, resulting in the persistent threat of further closures of domestic copper production facilities and the shrinking of our ability to meet national security production requirements.”

Many of the copper development projects in the US aim to produce copper cathodes, rather than concentrates, as they will utilise leaching and SX-EW processes. Project developers in Arizona are among the potential winners of Trump’s copper push, as the state has several copper projects nearing the construction phase, including Resolution, a joint venture between BHP and Rio Tinto (LSE:RIO); Taseko Mine’s (TSX:TKO) Florence; Hudbay Mining’s (TSX:HBM) Copper World; Arizona Sonoran Copper’s (TSX:ASCU) Cactus; Ivanhoe Electric’s (TSXV:IE) Santa Cruz; and Faraday Copper’s (TSX:FDY) Copper Creek. BHP also has the legacy assets of Kalamazoo, San Manuel, Copper City and Old Dominion that could be brought back into production.

To help projects along, the Trump administration is seeking to accelerate permitting timelines, which he has stated in his Energy Emergency executive orders when he took office in January 2025, and which sees the SPEED bill advance, (see RIN #8). This passed the House of Representatives on December 19, 2025.

Efforts to debottleneck the pipeline include efforts to ensure the development of the Ambler Mining District Access Road in Alaska, giving a green light for the development of the 40Blb Resolution copper project in Arizona, a joint venture between Rio Tinto and BHP, although court challenges continue to stall its progress, and the creation of a the FAST-41 dashboard to coordinate the project evaluation activities of federal permitting agencies, to remove slack time. Newrange Copper Nickel’s NorthMet project in Minnesota was added to FAST-41, for example. The Trump administration's commitment can go beyond this. In October 2025, the US government said it would take a 10% interest in Alaska copper developer Trilogy Metals (TSX:TMQ), and the federal government is providing funding backstops via the US Export-Import Bank (EXIM), to provide cheaper capital.

While beneficial for developers in the US, such moves, although positive, are disruptive because they cause major mining companies to wait and see how things unfold. In simple terms, the possibility of being subsidized to invest in the US means they hold investment decisions elsewhere. The 40Blb Resolution project is almost ready for development, which means BHP and Rio Tinto may decide to invest billions there rather than elsewhere.

Exhibit 6: Getting RIGI with it: (left to right) Michael Meding, Javier Milei, Rob McEwen

Source: Michael Meding

Argentina

Another disruptive presence is Argentina’s president, Javier Milei, who is adamant that his nation will become a large copper producer. Milei seeks to incentivize this through the RIGI incentive scheme for large investments that seeks to overcome the variable fiscal and legal conditions that have largely deterred investors for decades. Among the benefits the RIGI status confers upon a project is 30-year tax stability, including an overall tax burden that, depending on the project, falls from about 55% to 37-38%. It removes capital controls on earnings, provides for immediate VAT recovery, among other benefits. The owners of mining projects with multiple-decade lives do not want their in-country business conditions to change every time a new president takes office, particularly given Argentina’s recent challenging economic history.

The success of RIGI could reshape global copper investment flows. McEwen Copper, with its Los Azules project, may be the first copper mine built under RIGI (see Exhibit 6), with Glencore’s (LSE:GLEN) MARA project also a contender. Other potential beneficiaries are Lundin Mining (TSX:LUN) with its Vicuña JV with BHP (LSE:BHP), and Aldebaran Resources (TSXV:ALDE). Here is Michael Meding, VP and general manager of McEwen Copper:

“RIGI recovers the lost trust in Argentina. The mining investment law from the 1990s was a very good instrument at the time, but unfortunately, it wasn’t that well respected. Over the years, Argentine administrations circumvented it, and unfortunately, it wasn’t able to stand up in certain cases. RIGI is much clearer and will be much more difficult to circumnavigate.”

The power of RIGI could be magnified by the critical minerals agreement Argentina signed with the US in early February. The agreement establishes a partnership aimed at accelerating the development of secure, diversified, and resilient supply chains that are essential to technological innovation, industrial competitiveness, and national defense. The participants will jointly identify priority projects and facilitate their financing within six months, creating a sustainable long-term partnership based on fair market pricing. Argentina has several copper projects approaching the investment stage, including McEwen Copper’s Los Azules in San Juan. Under the bilateral agreement, projects in Argentina may be able to access financing from US EXIM Bank and US International Development Finance Corporation. Here is US Secretary of State, Marco Rubio:

“Because of the resources available and because of the investment capacity and processing expertise, I believe Argentina will be a key partner for the world—not only for the US.”

The potential of RIGI could be seen later this year if Lundin Mining and BHP start the 3.25-year development of their Vicuña Cu project in San Juan, which they just announced an integrated PEA on. Vicuña comprises the Filo del Sol and Josemaria deposits. A staged approach will see a sulphide mill developed for Josemaria. A second stage will develop the Filo del Sol leachable oxides with a SX/EW plant. A third stage will expand the concentrator to develop the Filo del Sol sulphide deposit, enabling peak production. Vicuña will produce an average of 400ktpy Cu, 700kozy Au & 22Mozy Ag over the first 25 full years of operation, with a mine life of more than 70 years. The first stage has a capital cost of US$7.1B, giving it a capital intensity of less than US$ 30,000/t of copper equivalent. Capital for the second and third stages is estimated at $11.1B.

British Columbia

Above, we have two initiatives that should be positive for copper developers. A look at British Columbia in Canada shows some potential risks emerging. British Columbia hosts several copper-gold porphyry exploration projects, which tend to be lower-grade than those in Chile and Peru. The higher metal prices environment somewhat overcomes their marginality, benefiting companies such as Kodiak Copper (TSXV:KDK), NorthWest Copper (TSXV:NWST), and others.

A more difficult bridge to cross for developers in British Columbia is that it is unceded territory, meaning that First Nations must be consulted about mineral developments in their territories and effectively have a veto. This stems from a modernization of the province’s Mineral Tenure Act (MTA) and the Declaration on the Rights of Indigenous Peoples Act (DRIPA), which saw the provincial government incorporate the United Nations Declaration on the Rights of Indigenous Peoples (UNDRIP). Among other things, since March 2025, this requires the province to conduct pre-consultation with First Nation groups when claims are staked, rather than automatically registering them. Developers face the possibility of additional time and cost to advance and obtain permits for their projects, as well as permitting uncertainty. For example, in August 2023, the Tahltan Nation opposed Torr Metals’ application for the Latham copper-gold project. In 2024, after years of deteriorating relations with the Tŝilhqot’in Nation, to exit the situation, Taseko Mines signed an agreement with them that their consent must be obtained for any future exploration and/or mine development at its New Prosperity copper-gold mine, with Taseko agreeing to walk away (with C$75M in compensation from the province).

More recently, Skeena Resources (TSX:SKE) negotiated an impacts and benefits agreement with the Tahltan Nation for its Eskay Creek Au-Ag project in the Golden Triangle, which features considerable financial benefits with aggregate cash payments of $1.2B over the mine’s life as well as $570M in contracts and wages. This has led to accusations of buying consent, pay-to-play and so on. First Nations increasingly recognise copper as critical, giving them additional negotiating leverage. It is likely safe to assume that the cost of obtaining their consent will increase, which for economically marginal projects, may be fatal. Joe Mazumdar of Exploration Insights gave an excellent overview of the state of affairs in his December 14 2025 issue. He concluded:

“I don’t expect these changes to materially impede development projects, unless there is a fundamental breakdown in the relationship with the local FN. … When choosing the right portfolio, the straightforward takeaway is that investing in British Columbia-focused resource companies now carries more risk than it used to.”

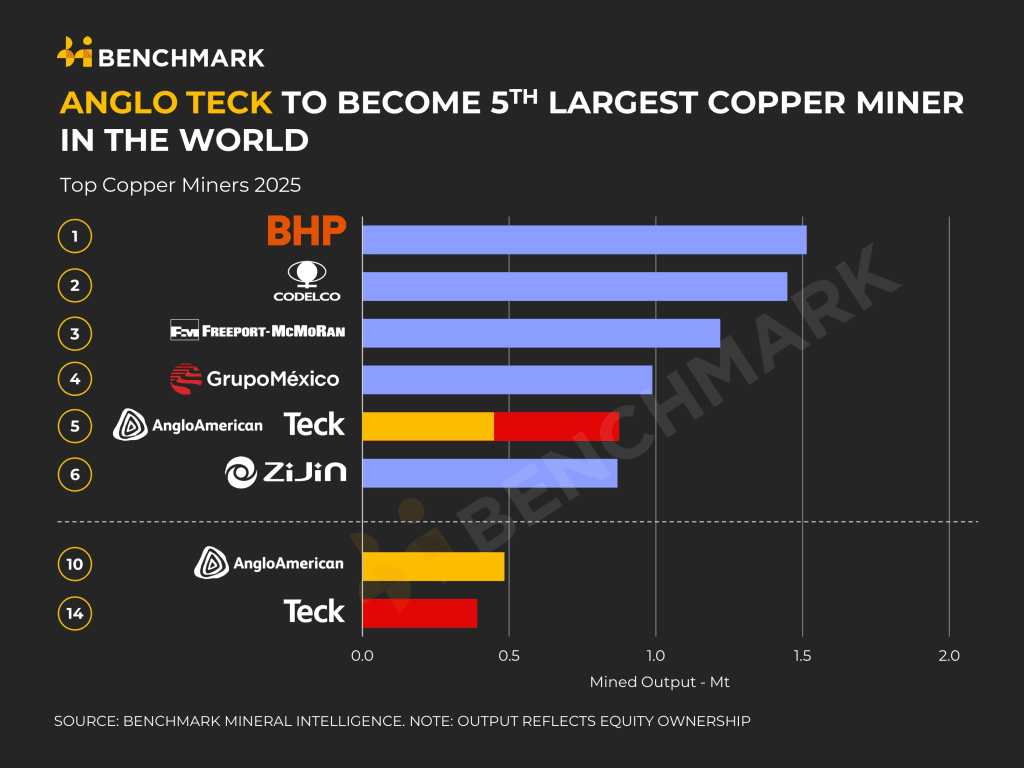

Exhibit 7: Few Large Copper Miners, Few Consolidation Options

Source: Benchmark Mineral Intelligence

Developers on the block

BNEF said major mining companies have begun to prioritize capital expenditure over shareholder distributions, with explosive copper demand emerging as a central driver in this reorientation. The $53B merger between AngloAmerican and Teck Resources to create one of the world’s largest copper producers (see Exhibit 7) is emblematic of this, as it will bring together the Collahuasi and Quebrada Blanca assets in Chile. Anglo American is also teaming with Codelco for the Los Bronces and Andina copper mines. Large M&A signals copper’s growing strategic value; however, buying growth does not increase the overall pool of copper available, and companies may be communicating that it is easier (and cheaper) to buy new capacity than build it themselves. Here is Robert Friedland speaking at the Indaba Conference in South Africa, mid-Februar,y referencing Barrick Mining (gold) and Rio Tinto (iron ore) in particular:

“Iron ore miners want copper. Gold miners want copper. It’s copper, copper, copper.”

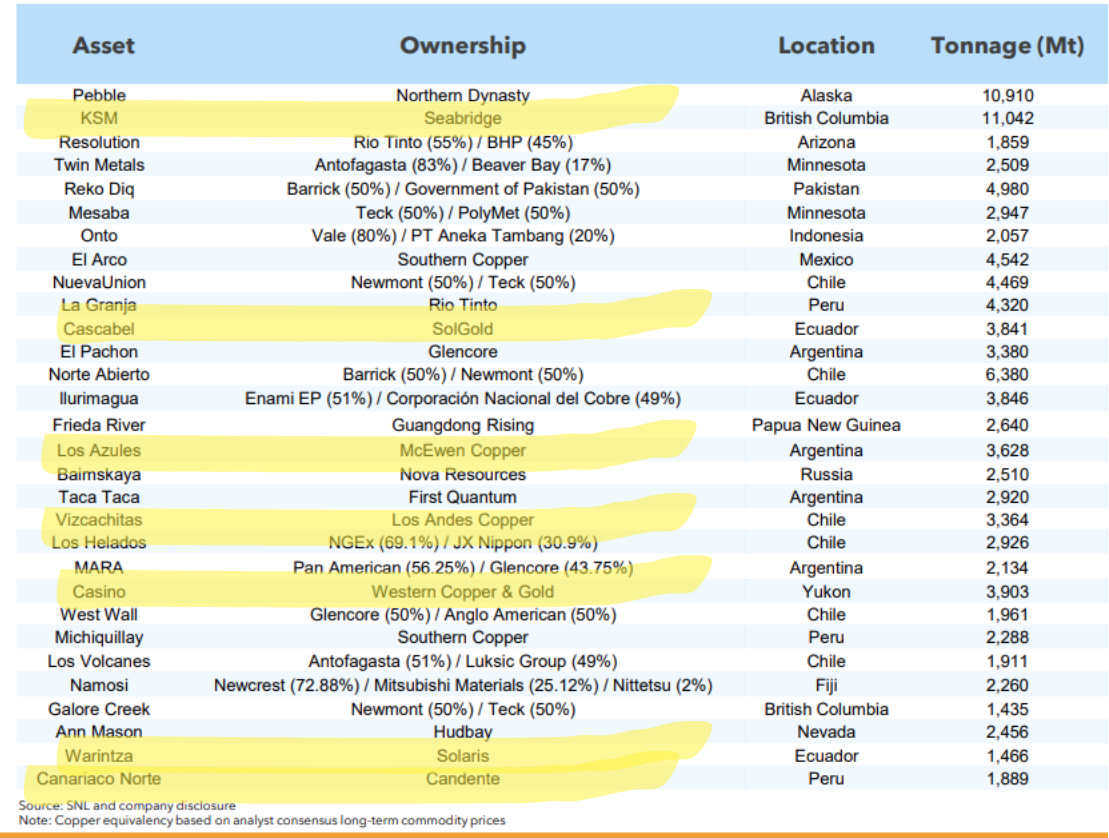

Exhibit 8: Copper Development Projects

Source: SNL

With comparatively few players in the copper sector (see Exhibit 8), there is only so much card shuffling that can be undertaken before majors need to buy juniors and develop new mines. There are also relatively few choices. Exhibit xx shows the main undeveloped copper projects, with those held by juniors highlighted. Two of these (Cascabel and Cañarico are subject to takeover bids. In November 2025, Jianxi Copper made three bids for Ecuador developer SolGold (LSE:SOLG), with the company’s board accepting an all-cash acquisition offer of £867M at a 42.9% premium in late December. This deal addresses the shortage of copper concentrates, as China’s smelters are having to offer zero TC/RCs to secure supplies. Jiangxi is one of China’s biggest copper smelters. Meanwhile, Fortescue (ASX:FMG) is taking out Alta Copper (TSX:ATCU) for its Cañariaco project in Peru.

With the copper price ending 2025 at $5.30/lb and 2026 promising to be a year of supply deficit, bids for other projects are likely. Although there are few buyers, producers have pipelines to fill and there are few options available.

Bioleaching

Let’s end with some potential for disruption. Part of the reticence of large copper miners to both build new projects and buy developers, in addition to extended permitting times, risk, and financial size, is the lack of clarity about the extent to which bioleaching of low-grade and complex copper ores will be possible. Porphyry copper deposits contain a vast amount of rock with a grade profile that softens as you move away from the core. Currently, a grade of 0.4% is economic and 0.3% is marginal. There is a lot more rock at 0.3% than 0.4%. There is even more at 0.2%, so you can understand that if bioleaching makes it possible to recover copper from such rock economically, the amount of rock that can be included in resources can jump significantly. A March 2024 report by Goldman Sachs said primary sulphide leaching could boost the production of the leading five producers by an aggregate 1Mtpa. All of the major copper producers, including Rio Tinto, Glencore, Freeport-McMoRan, and Antofagasta, are working on the challenge, as are private companies such as Jetti and Ceibo. Freeport-McMoRan is probably the most successful to date, seeking to produce 800,000tpy. New players are emerging, such as Endolith Mining, which is working with BHP and Rio Tinto. Endolith sees a 1.7-1.9x improvement in copper recovery across more than four low-grade ore types, including chalcopyrite and bornite, bringing the possibility to drop cut-off grades below 0.3% copper. Here is Endloith founder and CEO, Liz Dennet:

“We are not looking to deploy just one microbe: we are looking at heap engineering and creating a unique microbial platform. Just putting bugs in a heap doesn’t scale. The capex and opex is not there. There are dozens of different microbial communities in a heap. … Only now can we listen to them and get them to do what they need to do. It is about understanding them within microbial communities and optimising these communities to function in high-salinity, high-arsenic, and other extreme environments, as well as at different temperatures. We help them catalyse their redox reactions,” said Dennett.

Before we get to some specific companies, please note that the aim of the RIN is to continue to build your knowledge and understanding of mining investment themes, and is to be used in conjunction with the Rule Classroom, the Rule Bootcamps, the Rule Investment Media YouTube channel, and, of course, the annual Rule Symposium.

As a quick reminder, registration is now open for the 2026 Rule Symposium in Boca Raton, Florida, from July 6 to 10, 2026. The event will feature new participants, including the Lundin Group and Allied Gold, among others. To register, click the button below.

Investor options

There are many options for investors to get exposure to copper. A simple way is the Sprott Copper Miners ETF (COPP), which invests in a diversified portfolio of copper-related companies. From blue-chip names such as Freeport-McMoRan and Antofagasta to non-producing developers, including Regulus Resources and Marimaca Copper. In RIN we focus on smaller companies where we see opportunities, hence we will not be talking about the copper majors here.

Ivanhoe Mines (TSX:IVN) www.ivanhoemines.com

Key investment highlights:

Producer in DRC

Robert Friedland owns 11.5%, Zijin Mining owns 12.2%, CITIC Metal owns 21.3%

Overcoming Kakula mine incident

Growing copper (and other metals) production profile

Cash US$1.1B (Sept 2025)

Ivanhoe Mines is bouncing back after suspending mining in May 2025 at the Kakula underground mine at its Kamoa-Kakula complex in the Democratic Republic of the Congo, following seismic activity that damaged underground infrastructure and raised water levels. This saw it cut its 2025 guidance by 28% from 520,000-580,000t of copper to 370,000-420,000t. The company has guided a similar production range of 380,000-420,000t in 2026, despite ongoing risk factors, and anticipates an increase to 500,000-540,000t in 2027. An updated life-of-mine plan is due in the March quarter of 2026 at a processing rate of 17Mtpy, with a phase four expansion on the cards to add another 6.5Mtpy to processing capacity. The company’s medium-term production target is about 550,000tpy. The company has significant exploration potential in the Western Forelands.

Ivanhoe also operates the Kipushi zinc mines, which also produce copper, silver and germanium in DRC and the Platreef PGM-nickel-copper mine in South Africa.

Ero Copper (NYSE:ERO) www.erocopper.com

Key investment highlights:

Producer in Brazil, where Tucama mine ramping up in 2026

Gold kicker from Xanvantina

JV relationship with Vale Base Metals, Furnas PEA in 2026

Paul Harris did a site visit in 2022

Cash US$66M (Sept 2025)

2025 was a landmark year for Ero Copper, which saw its Tucumã copper mine development in Para, Brazil, achieve commercial production, which is expected to increase production to more than 50,000tpy, with more to come as it advances its Furnas JV project with Vale Base Metals, with a PEA due in 1H26. High metal prices enable the company to rapidly pay down debt, with its net debt leverage ratio (net debt:EBITDA) declining from 2.4x in 2024 to 1.9x by late 2025. The goal is to achieve a ratio of 1-1.5x by 2026. Here is chief executive Makko DeFilippo:

“We have several years before we need to make major capital deployment on construction [of Furnas], we have sequential record quarters of production, and high metals prices, so we would like to get to the point where we can give excess cash back to shareholders. It is important for us to demonstrate capital discipline.”

Amerigo Resources (TSX:ARG) www.amerigoresources.com

Key investment highlights:

Copper cathode producer in Chile

Robust, multi-decade operation

Strong dividend and share buyback program

Paul Harris did a site visit in 2019

Cash US$31.1M (Sept 2025)

Amerigo is a unique company in that it reprocesses fresh and historical tailings from Codelco’s El Teniente mine in Chile. This means it has a straightforward and reliable business plan, which, in the current metal price environment, makes it something of a cash cow, and it shares this with shareholders via dividends. In 2025, the company repaid its debt and increased its dividend from 3c to 4c per share, as it seeks to return more of its free cash flow to shareholders. Here is president & CEO Aurora Davidson:

“Reaching debt-free status was one of our stated objectives for 2025 and concludes a strategic ten-year period for the company. The company’s quarterly dividend has now been increased to 4c per share, which is roughly 50% of the annual additional free cash flow that will become available from not carrying debt.”

McEwen Copper via McEwen Inc (NYSE.MUX) www.mcewenmining.com

Key investment highlights:

Advanced-stage project in San Juan, Argentina to produce copper cathode

Possibly the next large project into production

Accepted into RIGI tax-legal stability program

Rob McEwen major shareholder, insider ownership 17%

Paul Harris did a site visit in 2024

Cash US$51M (Sept 2025)

McEwen Copper’s Los Azules project may be the next greenfield copper development. An October 2025 Azules feasibility study detailed the production of 148,200tpy of copper cathode for 21 years at a C1 cash cost of US$1.71/lb. The project will yield an after-tax NPV8 of US$2.9B, an internal rate of return of 19.8% and a 3.9-year payback at a $4.35/lb copper price following an initial capital investment of $3.17B, giving it a capital intensity of $20,200/t of annual production. At a $5/lb copper price, these improve to $4.5B, 25% and 3.2 years. With McEwen seeking to start construction as early as late 2026 or early 2027, financing the development is the company’s main goal in 2026. McEwen Copper is a subsidiary of gold producer McEwen Inc, which originally considered spinning McEwen Copper out into a separate publicly-listed company. The increase in metals prices and subsequent increase in the market capitalisation of McEwen Inc. reduce the need to spin out McEwen Copper from a financing perspective but still make sense from an eventual monetisation exit strategy perspective. Here is VP and general manager, Michael Meding:

“We have seen significant interest from export credit agencies and export development banks. Last week I was on a site visit to the project with 46 visitors that are looking into copper space, including many that have a clear interest in financing either equipment or the project itself.”

Arizona Sonoran Copper (TSX:ASCU) www.arizonasonoran.com

Key investment highlights:

Share price change YoY 228%

Advanced-stage US cathode project

Rio Tinto and Hudbay Minerals strategic shareholders

Near surface, low cost

FS in 2H26

Paul Harris did a site visit in February 2023

Cash US$103M (Dec 2025)

Arizona Sonoran Copper could be the next project advancing to an investment decision as it works towards producing a simplified prefeasibility study (PFS). The company recently completed the PFS drilling with the study to produce 100,000tpy of copper cathode from a conventional open pit, heap leach and SX-EW operation. It expects to obtain permits for a development in about a year and, following completion of a PFS and a feasibility study, to be able to make an investment decision by the end of 2026. Cactus contains an estimated 11Blb of measured and indicated copper, including 5.3Blb of reserves grading 0.52% copper.

The company recently raised C$80M, including a cornerstone investment from Hudbay Minerals to take a 9.9% stake, and it reduced project risk by repurchasing some of the royalties on it, and adding to its land position. Company officials have engaged with the US government to gauge interest in federal funding for Cactus, which will produce copper cathodes. The company also just announced it will pay US$20M to Rio Tinto subsidiary Nuton to terminate the latter’s option to JV Cactus, and another $15M if Arizona Sonoran is taken out within two years of the termination. Here is president & CEO, George Ogilvy:

“Buying those royalties back added tens of millions of dollars of accretion for the shareholders of the company. If the pundits are right that the copper price is going significantly higher, we’re talking hundreds of millions of dollars of accretion to the shareholders of the company and not the royalty companies.”

Faraday Copper (TSX:FDY) www.faradaycopper.com

Key investment highlights:

Advanced-stage US cathode project

Lundin Group backing

18 months from investment decisions

Paul Harris did a site visit in February 2023

Cash C$45.9M (Sept 2025)

Faraday Copper raised C$49M in July 2025 to continue advancing its Copper Creek project in Arizona. The company estimates it will take about 18 months of work to get to an investment decision, with a 40,000m drilling programme underway to grow resources with a view of being ready to submit a mine plan of operations in the March quarter of 2027. Here is president & CEO, Paul Harbidge:

“We were working for two years under the last administration to get this, and within six months of Trump it was approved. Our drilling is now fully permitted to get to a final investment decision. … We have to take advantage of this administration to permit.”

Ivanhoe Electric (NYSE-A/TSX:IE) www.ivanhoeelectric.com

Key investment highlights:

Advanced-stage US cathode project

Robert Friedland company

US EXIM $825M debt possible

Cash US$235M (Oct2025)

Ivanhoe Electric, backed by Robert Friedland, is attracting interest in Washington as the only American company. In April 2025, they lined up a possible $825M financing with US EXIM. It issued a PFS in June 2025 for average production of 72,000tpa of copper cathode during the first 15 years of a 23-year life, with mine construction to start in the first half of 2026, with project capital estimated at $1.24B. Here is a company official:

“We have a lot of wind in our sails. We are at the tip of the spear in DC for new copper stories.”

Regulus Resources (TSXV:REG) www.regulusresources.com

Key investment highlights:

Advanced-stage project in Cajamarca, Peru

Robust, multi-decade operation

Rio Tinto owns 16.11%

Potential Rio Tinto Nuton upside

Consolidation potential with majors

M&A experience

Paul Harris did a site visit in 2017

Cash C$10M (Dec 2025)

Regulus Resources is exploring the advanced-stage AntaKori copper-gold project in Cajamarca, Peru that has an indicated resource of 250Mt @ 0.48% Cu, 0.29g/t Au & 7.5g/t Ag containing 2.6Blb Cu, 2.3Moz Au & 61Moz Ag, with another 267Mt of inferred resources containing 2.4Blb Cu, 2.2Moz Au & 67Moz Ag. AntaKori is part of a larger deposit called Tantahuatay mined by its neighbour Coimolache, a subsidiary of Peruvian miner Buenaventura and Southern Copper. Regulus and Coimolache have been working on an integrated sulphide project resource estimate and PEA, but it is unclear whether these will be publicly released. Testing with Rio Tinto’s Nuton’s bioleach process is yielding positive results, particularly with the enargite-rich high-sulphidation mineralisation that makes up the bulk of AntaKori mineralisation.

AntaKori is a takeover target as it is within a district with several active larger players, most of whom see their existing operations winding down in the coming years. The M&A question is when, not, if, and by whom? Antofagasta acquired a 19% stake in Buenaventura and is seeking to expand its presence in Peru. Gold Fields is also in the picture as its nearby Cerro Corona gold mine is nearing the end of its life. This is a rodeo the management team successfully participated in during the last copper cycle, when it sold Antares Minerals to First Quantum Minerals for C$650M. Here is president & CEO John Black:

“Conditions have been established under which attractive copper extraction is achieved from both high-sulphidation and porphyry mineralisation utilising Nuton’s bioleaching technology. With several other columns underway, we continue to view Nuton’s bioleaching technology as one of several potential processing options for mineralisation at AntaKori.”

Aldebaran Resources (TSXV:ALDE) www.aldebaranresources.com

Key investment highlights:

Advanced-stage project in San Juan, Argentina

Next to Los Azules, infrastructure benefit

Potential Rio Tinto Nuton upside

South32 owns 14.81%, Sibanye Stillwater owns 14.34%

Los capital intensity

M&A experience

Cash C$13M (Sept 2025)

From the same management team as Regulus Resources, Aldebaran Resources announced a PEA for its Altar copper-gold project in San Juan, Argentina in October 2025, with a base case 60,000tpd concentrator to process material from both open pit and underground sources. Altar will produce an average of 92,891tpy Cu, 27,020oz/y Au & 525,192oz/y Ag, or 101,413t CuEq for more than 40 years at a C1 cash cost of US$2.02/lb following an initial capital investment of US$1.59B, giving the project a capital intensity of $15,713/t. During its first 20 years, it would average 121,445tpy CuEq. Upfront capital is minimised by taking a staged approach to the tailings storage facility and underground construction. The project would yield an after-tax NPV8 of $2B, an IRR of 20.5%, and a four-year payback, using base-case metal prices of $4.35/lb Cu, $2500/oz Au, and $27/oz Ag. These improve to $3.34B and 28.0% at $5/lb Cu, $3963/oz Au & $47/oz Ag. Opportunities include the installation of a molybdenum recovery circuit, additional metallurgical testing to potentially improve copper recoveries, and Nuton technology scenario. The use of Rio Tinto’s Nuton leach technology would reduce life-of-mine capital expenditure and operating costs, leading to higher life-of-mine free cash flow. Aldebaran is preparing to apply for inclusion under Argentina’s the Large Investment Incentive Regime (RIGI) fiscal regime, and an updated resource estimate. The management team successfully executed M&A during the last copper cycle, when it sold Antares Minerals to First Quantum Minerals for C$650M. Here is president & CEO John Black:

“We hit a sweet spot of a mine size to be of interest to a copper company, but it could be scaled. This gives us more flexibility on potential suitors by providing a simpler and quicker pathway to get into production. We don’t want to over-scale something.”

Solaris Resources (TSX:SLS) www.www.solarisresources.com

Key investment highlights:

PFS-stage project in Ecuador

Low capital intensity

District potential underpinned by core resource

Redomiciled to Switzerland to open door to China company deal

Cash US$35M (Sept 2025)

Solaris completed a prefeasibility study for its Warintza copper-gold development project in southern Ecuador in November 2025, and aims to complete the permitting process by the end of 2026. The study detailed average annual copper equivalent production of 240,000tpy for the first 15 years at a C1 cash cost of US$1.07/lb, with an after-tax NPV8 of $4.6B and an IRR of 26% following an initial capital investment of $3.7B, an attractive capital intensity of about $15,440/t. Warintza hosts about 1.3Bt of reserves and 5.8Bt of resources in a near-surface deposit with a low strip and conventional processing. An early infrastructure works programme began a year ago, funded by a $200M raise from Royal Gold. Solaris has the funds to complete a feasibility study and advance to a final investment decision in late 2026. The adverse financial situation of Ecuador, combined with a business-friendly president, should bode well for the project. Nearby developments, such as Lundin Gold’s Fruta del Norte gold mine, have shown that mines can be developed in the region that manage environmental and community aspects well.

NGEX Minerals (TSX:NGEX) www.ngexminerals.com

Key investment highlights:

Advanced-stage copper-gold-silver project in San Juan, Argentina

Very high grade with gold and silver

Lundin Group company

Cash C$121M (Sept 2025)

The Lunahuasi project in San Juan, Argentina, is anomalously well-endowed with metals, with eye-popping drill results including 60m grading 7.52% copper equivalent, 23m grading 23.02%, 38.9m grading 10.84% and 51.1m grading 13.84%. Multiple waves of mineralization brought copper, gold and silver into the system. As impressive as the copper numbers are, the high-grade gold component differentiates Lunahuasi from other deposits in the Vicuña district, such as Filo and Josemaria, which are in a JV between BHP and Lundin Mining. The deposit may also be rich enough for NGEx to develop without a bigger partner. Drilling has defined a mineralised area of 1.1km by 1.2km by 1.2km depth, which is near surface and continues to expand. High-grade material may only require a 300-400m adit to get into, compared with the greater depths other deposits are at. In 2026, the company aims to complete a 25,000m Phase 4 drill program, obtain permits and begin development of an exploration adit, and submit an application to be included in the RIGI tax and legal stability program. In late 2025, the company spun out a net smelter returns royalty on Lunahuasi and the Los Helados project in Chile into LunR Royalties (TSXV:LUNR) in which it retained a 19.9% ownership interest. The company also owns the Los Helados project in Chile that hosts 18.4Blb Cu, 10.2Moz Au & 97.5Moz Ag. This is 17km from Lundin Mining’s majority-owned Caserones mine.

Marimaca Copper (TSX:MARI) www.marimaca.com

Key investment highlights:

Advanced-stage project in Chile

Near the coast, great infrastructure

Low capital intensity

Cathode production potential

New discoveries, exploration potential

Paul Harris did a site visit in 2019

Cash US$78M (Sept 2025)

Marimaca Copper has obtained environmental approval for its US$587M Marimaca oxide heap leach and SX-EW copper project in the Antofagasta region of Chile where an August 2025 feasibility study detailed the production of 43,000tpy of copper cathode for an estimated 13 years at a C1 cash cost of $2.09/lb following a $587M initial capital investment, with an average production of 50,000tpy during the first five years. It has a capital intensity of $13,651/t of annual production. The project, near Mejillones, will use seawater and renewable energy, with construction to begin in 2026. Exploration continues to deliver, to the extent that the company sees potential to expand future operations to 70,000tpy through the incorporation of the Pampa Medina and Madrugador oxide deposits. Here is MD Hayden Locke:

“There are few actionable copper projects out there, and you can see this in the price Hudbay got for Copper World,” Locke said. “We are not so small that we don’t move the needle for everyone but the majors. If we can expand to 70,000tpa cathode, that is meaningful for everyone below BHP, Antofagasta, Rio Tinto, First Quantum Minerals and Anglo American in an amazing location, in a tier one jurisdiction with relatively low execution risk and manageable capex.”

ATEX Resources (TSXV:ATX) www.atexresources.com

Key investment highlights:

Explorer in Chile

Backed by Pierre Lassonde and Agnico Eagle Mines

Near-surface B2B zone gives starter potential

Cash C$114M (Nov 2025)

In September 2025, ATEX Resources released an updated resource estimate for its Valeriano copper project in Chile’s Atacama Region, with an indicated resource of 475Mt grading 0.58% copper, 0.25gpt gold, 1.39gpt silver and 70.4gpt molybdenum, containing 6.Blb of copper, 3.8Moz of gold, 21.2Moz of silver and 33,000t of molybdenum. It also hosts inferred resources of 16.7Blb of copper, 9.9Moz of gold, 56.1Moz of silver and 107,000t of molybdenum. That adds up to more than over 9Blb of indicated copper equivalent and 25Blb of inferred copper equivalent.

Much of the deposit is relatively deep underground, which would require higher-cost development to exploit. However, the discovery of the B2B zone high-grade breccia closer to the surface, which hosts an indicated resource of 28.4Mt grading 1.36% copper equivalent, provides the possibility of a smaller starter underground mine that could pave the way for the exploitation of the main orebody with earlier and lower-cost production. Metallurgical testing has demonstrated copper and gold recoveries exceeding 95% in a low-impurity concentrate. In October 2024, gold major Agnico Eagle Mines (NYSE:AEM) invested US$40M for a 12% stake in the company.